Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

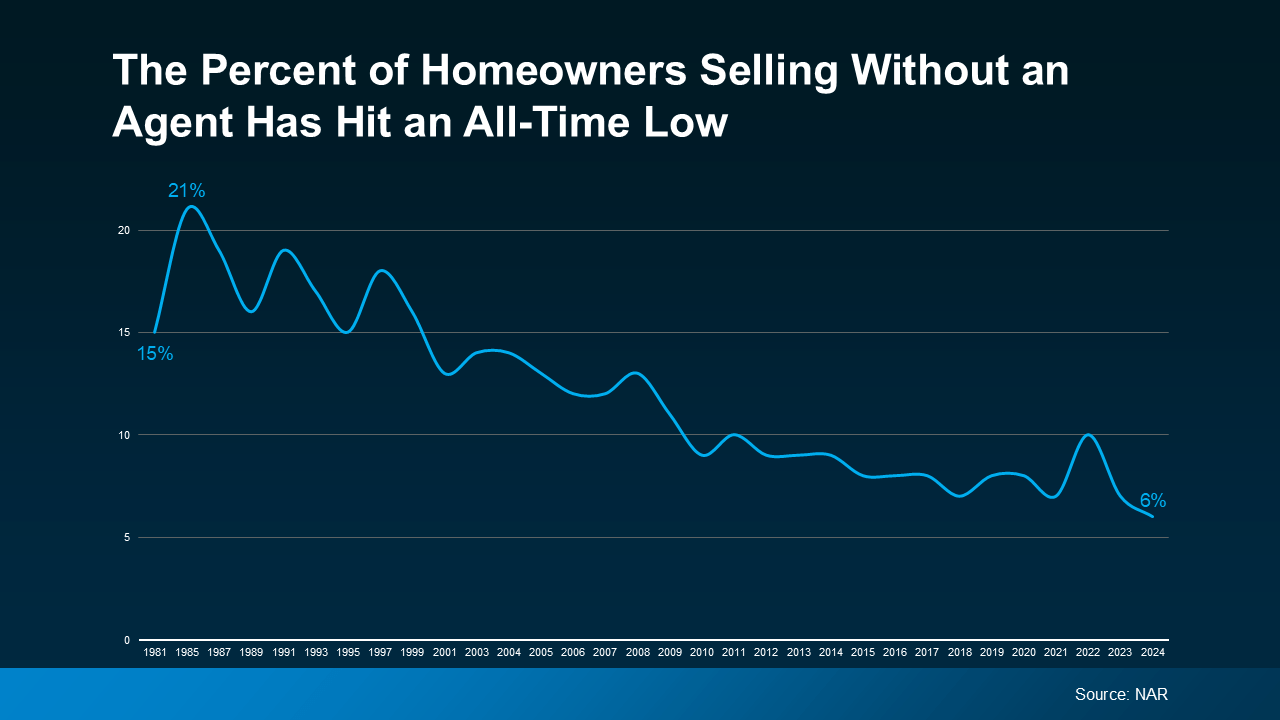

Selling your house without an agent as a “For Sale by Owner” (FSBO) may be something you’ve considered. But you should know that, in today’s shifting market, more homeowners are deciding that’s just not worth the risk.

According to the latest data from the National Association of Realtors (NAR), the number of homeowners selling without an agent has hit an all-time low (see graph below):

And for the small number of homeowners who do decide to sell on their own, data shows they’re still not confident they’re making a good choice.

And for the small number of homeowners who do decide to sell on their own, data shows they’re still not confident they’re making a good choice.

A recent survey finds three out of every four homeowners who don’t plan to use an agent have doubts about whether that’s actually the right decision.

And here’s why. The market is changing – not in a bad way, just in a way that requires a smarter, more strategic approach.And having a real estate expert in your corner really pays off.

Here are just two of the ways an agent’s expertise makes a difference.

1. Getting the Price Right in a Market That’s Evolving

One of the biggest hurdles when selling a house on your own is figuring out the right price. It’s not as simple as picking a number that sounds good or selling your house for what your neighbor’s sold for a few years back – you need to hit the bullseye for where the market is right now. Without an agent’s help, you’re more likely to miss the mark. As Zillow explains:

“Agents are pros when it comes to pricing properties and have their finger on the pulse of your local market. They understand current buying trends and can provide insight into how your home compares to others for sale nearby.”

Basically, they know what’s really selling, what buyers are willing to pay in your area, and how to position your house to sell quickly. That kind of insight can have a big impact, especially in a market that’s balancing out.

2. Handling (and Actually Understanding) the Legal Documents

There’s also a mountain of documentation when selling a house, including everything from disclosures to contracts. And a mistake can have big legal implications. This is another area where having an agent can help.

They’ve handled these documents countless times and know exactly what’s needed to keep everything on track, so you avoid delays. And now that buyers are including more contingencies again and asking for concessions, your agent will guide you through each form step by step, making sure it’s done right and documented correctly the first time.

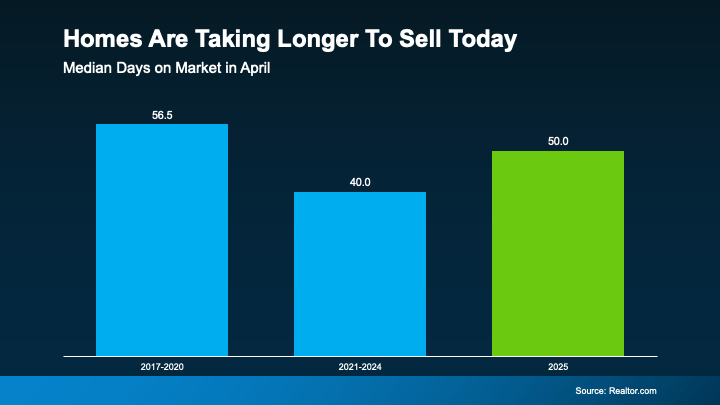

3. Selling Your House Quickly Even in a Shifting Market

Now that the number of homes for sale has grown, homes aren’t selling at quite the same pace they were. But you can still sell quickly if you have a proven plan to help your house stand out.

Just remember, homeowners don’t have the same network or marketing tools an experienced agent does. So, if you want the process to happen fast, you’ll likely want a pro by your side.

So, having the right agent and the right strategy is key in a shifting market. You know who to call! 🙂

And more homes for sale means more choices. There’s a good chance your perfect match just hit the market – or it will soon. So, it’s a great time to explore what’s out there. As Jake Krimmel, Economist at Realtor.com, says:

And more homes for sale means more choices. There’s a good chance your perfect match just hit the market – or it will soon. So, it’s a great time to explore what’s out there. As Jake Krimmel, Economist at Realtor.com, says:

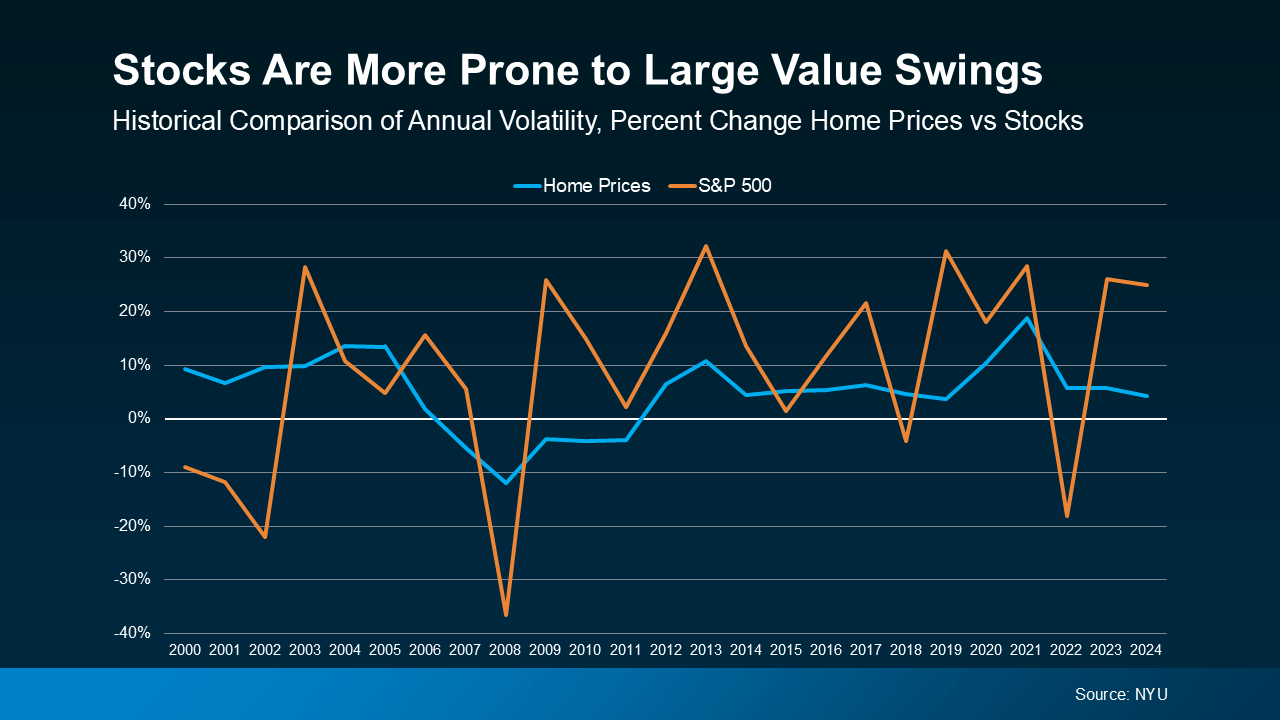

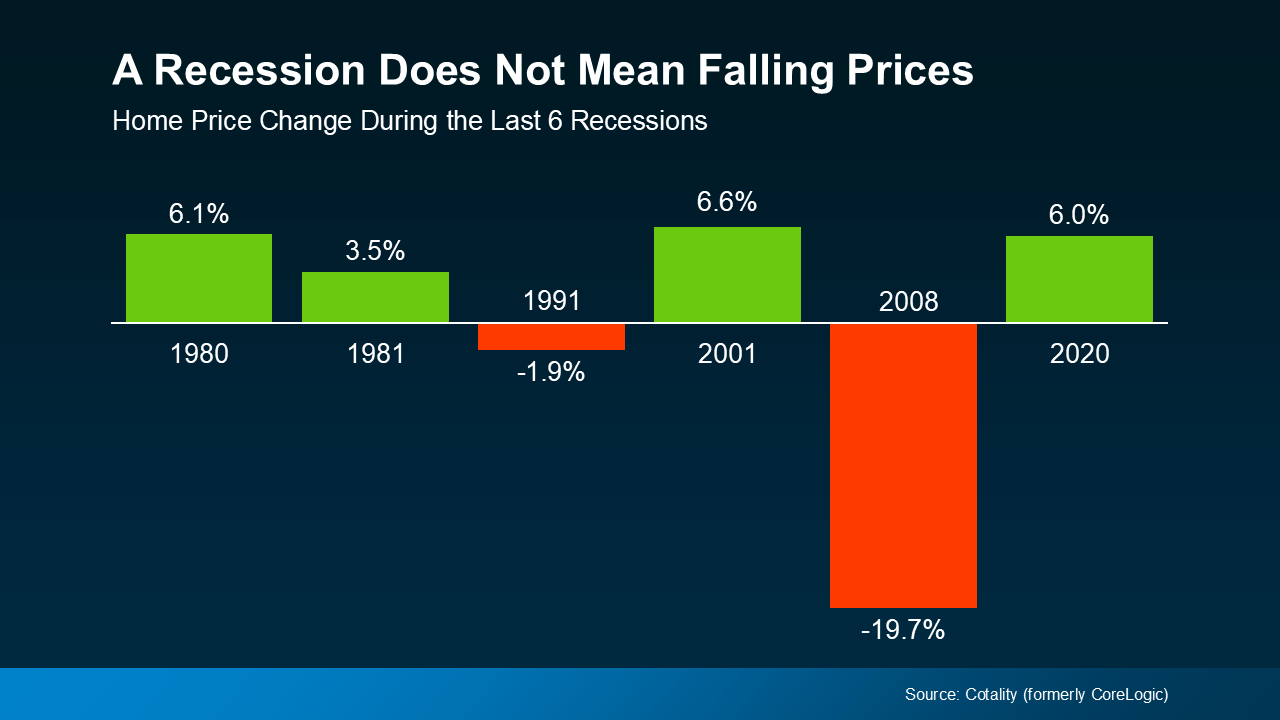

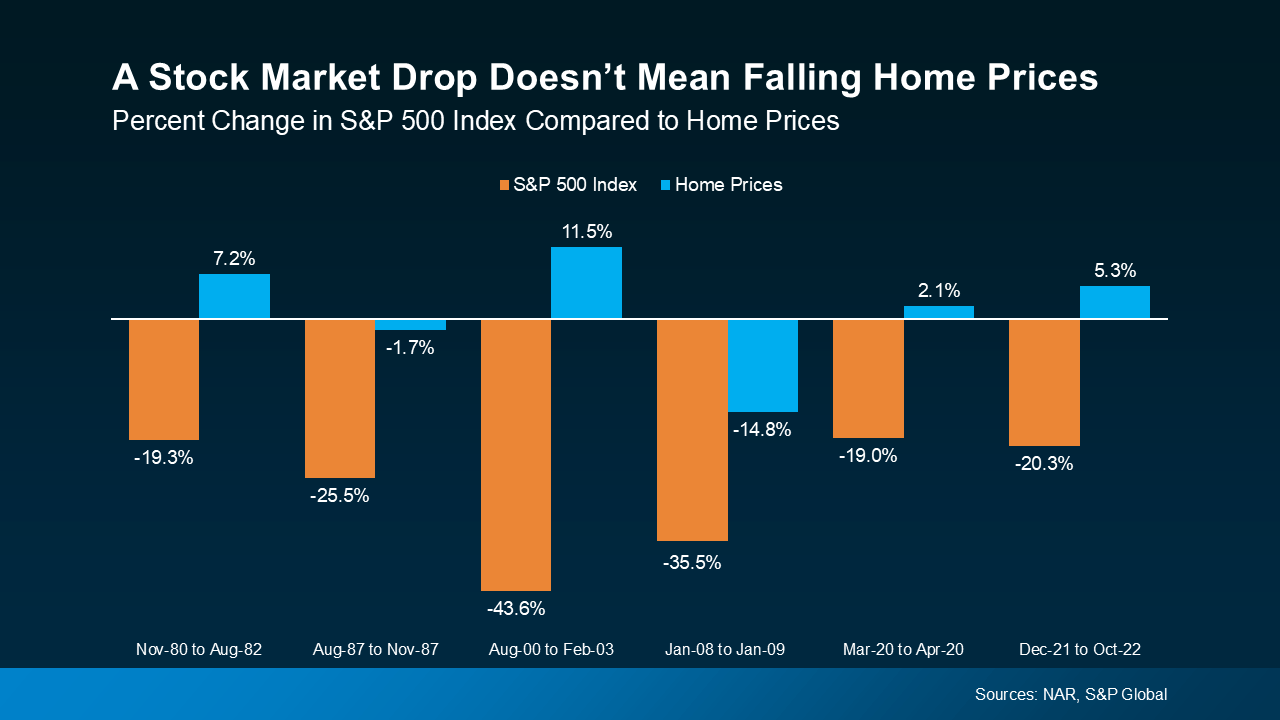

Even when the stock market falls more substantially, home prices don’t always come down with it.

Even when the stock market falls more substantially, home prices don’t always come down with it.