Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

A lot of people assume spring is the ideal time to sell a house. And sure, buyer demand usually picks up at that time of year. But here’s the catch: so does your competition because a lot of people put their homes on the market at the same time.

So, what’s the real advantage of selling your house before spring?

- It’ll stand out.

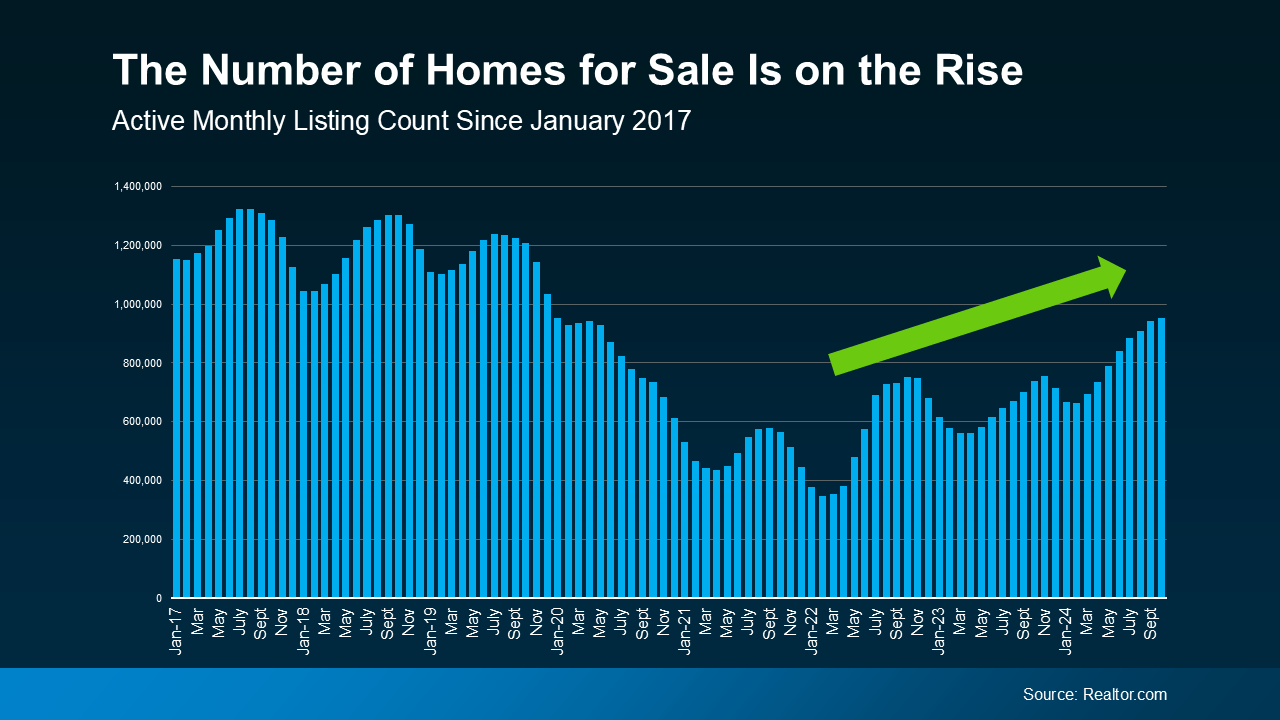

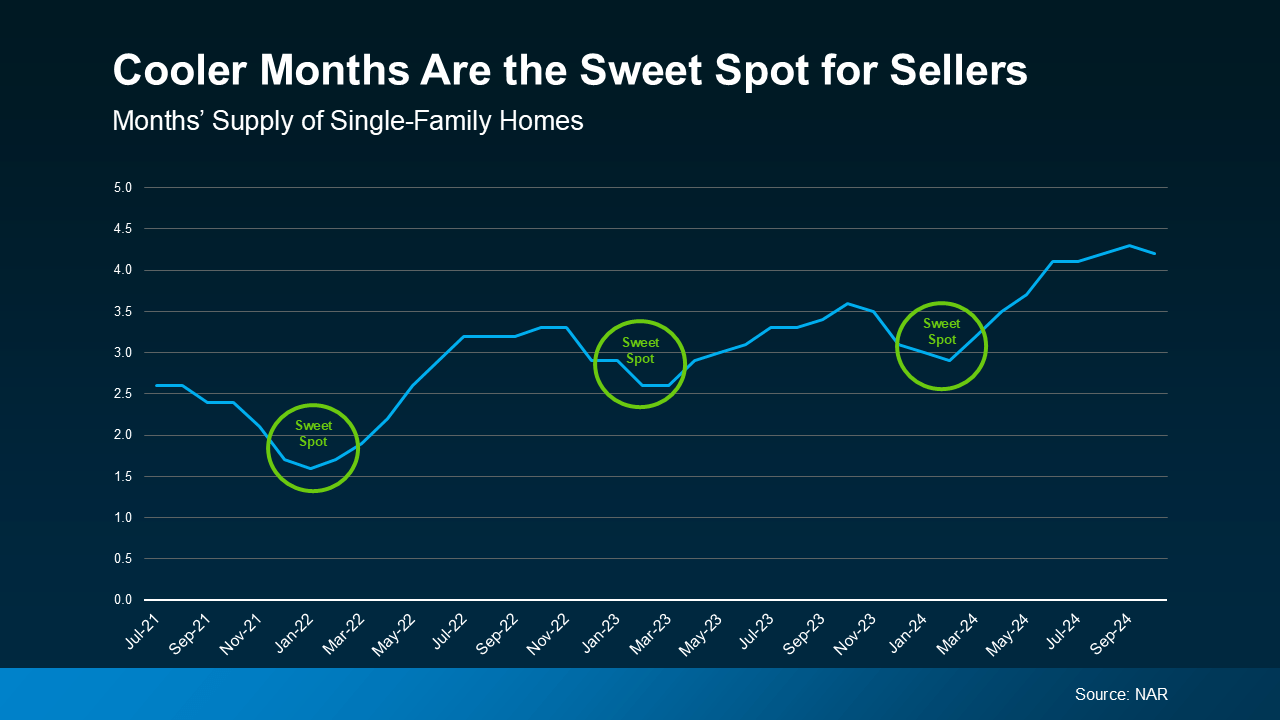

Historically, the number of homes for sale tends to drop during the cooler months – and that means buyers have fewer options to choose from.

You can see how that trend played out over the past few years in this data from the National Association of Realtors (NAR). Each time, the supply of homes for sale dipped during these cooler months. And then, after each winter lull, inventory started to climb as more sellers jumped into the market closer to spring (see graph below):

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent (me, of course) to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent (me, of course) to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

So, why wait until spring when you can get ahead of the curve now?

2. Fewer Listings Also Means More Eyes on Your Home

Another big perk of selling in the winter? The buyers who are looking right now are serious about making a move.

During this season, the window-shopper crowd tends to stay busy with other things, like holiday celebrations, and avoids looking for homes when the weather’s cooler. So, the buyers out looking aren’t casually browsing—they’re motivated, whether it’s because of a job relocation, a lease ending, or some other time-sensitive reason. And those are the types of buyers you want to work with. Investopedia explains:

“. . . if your house is up for sale in the winter and someone is looking at it, chances are that person is serious and ready to buy.”

So, with less competition and serious buyers on the hunt, you’ll be in a great position to sell your house this winter. Let’s connect if you’re ready to get the process started.

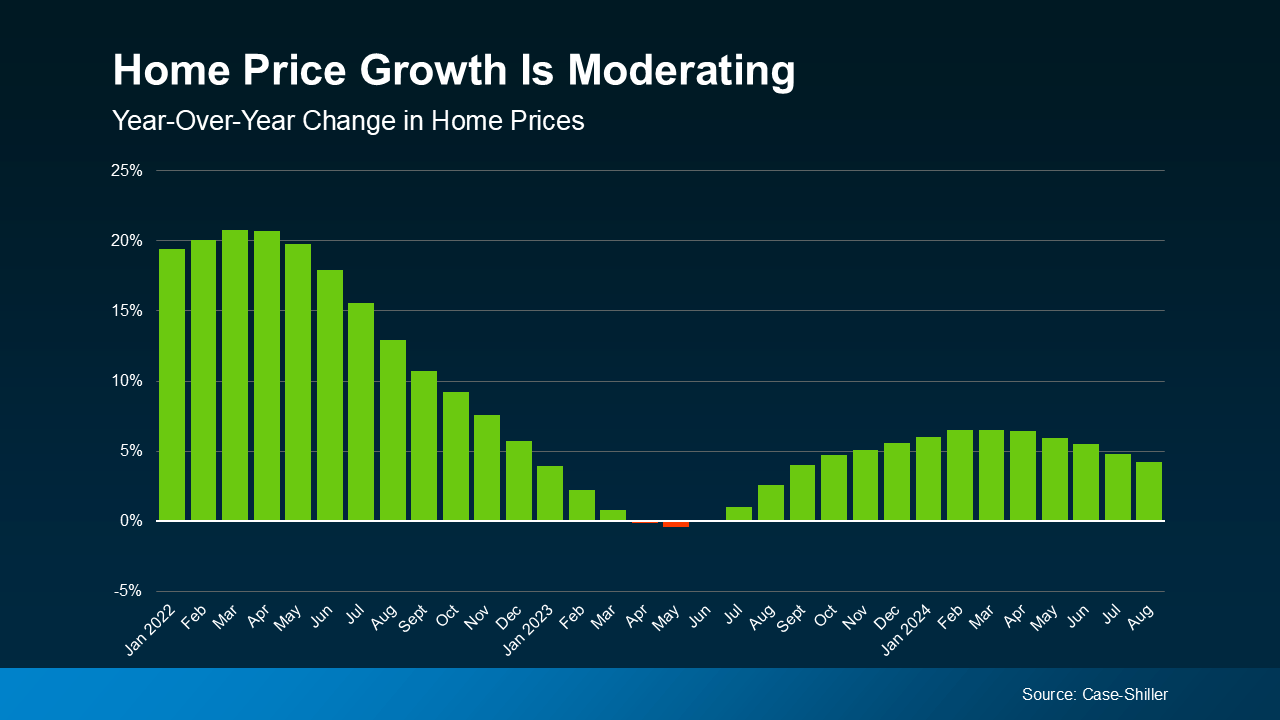

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.