Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Selling Your House •

November 12, 2024

What’s Motivating Homeowners To Move Right Now

Over the past few years, some homeowners have decided to delay their move because they don’t want to sell and take on a higher mortgage rate on their next home.

Maybe you’re thinking the same thing? It’s a common roadblock and one of the biggest factors that’s kept the number of homes on the market so low for so long.

But a growing number of homeowners are deciding they just can’t wait any longer. Often, it’s because of personal or lifestyle change. As Redfin says:

“Some homeowners are opting to bite the bullet and give up their low rate in order to move. Many are selling because a major life event like a job change, or divorce . . .”

If you’re weighing the decision to move, take a look at some of the top reasons others are choosing to sell. You might find those are reason enough for you to move now, too.

It’s Time for a Change

A new job in a different city, a desire to be closer to family, or simply wanting a change of scenery can all spark the need to sell.

Let’s say you’ve landed a great job offer that requires relocating, listing your current home quickly may be the next logical step.

There’s Just Not Enough Space in Your Current House

Sometimes, your current home just doesn’t fit your lifestyle anymore. A growing family, the need for a home office, or more room for entertaining can all drive the decision to upgrade to a larger space.

Retirement or Wanting To Downsize

On the flip side, some homeowners are ready to downsize. This could be due to children moving out, retirement, or simply wanting less to maintain.

If you’re newly retired and dreaming of a simpler lifestyle, downsizing to a smaller home could free up both time and resources to enjoy this new chapter of life.

Changes in Relationship Status

Big changes like divorce, separation, or marriage often lead to a need for new living arrangements.

If you just went through a divorce, selling the house you once shared may allow both of you to move forward and find a living situation that works better for you now.

Health and Mobility Needs

Health concerns, especially those that affect mobility, can also drive the decision to sell. A home that once worked well might no longer suit your needs.

If this sounds like your experience right now, selling your current home to move into a more accessible space, or even using the proceeds for assisted living, could significantly improve your quality of life.

So, selling your home isn’t just about market conditions or mortgage rates—it’s also about making the best decision for your lifestyle and future:

“Deciding whether it’s the right time to sell your home is a very personal choice. There are numerous important questions to consider, both financial and lifestyle-based . . . Your future plans and goals should be a significant part of the equation.” (Bankrate)

If a major life change has you thinking about moving, now might still be the right time to sell. Let’s connect so you have an expert to help you navigate the process.

Local Market Update •

November 12, 2024

Seattle Real Estate: Current Market Outlook

In today’s economy, understanding the latest numbers can give us valuable insights into where things are headed. Windermere’s Principal Economist, Jeff Tucker, keeps us updated on the local market with short, helpful videos.

Using Jeff’s transcript, I’m providing a written breakdown of his latest 4-min video, which you can watch here:

Here’s a local look at the October 2024 from the Northwest MLS. All in all, this month showed a strong performance in our local housing market, especially in the single-family residential segment.

To get a feel for our current market dynamics, let’s dig into 4 key market indicators: closed sales, pending sales, active listings, and median sales prices:

- Closed Sales: In October, residential closed sales climbed significantly, with an increase of over 1,000 transactions compared to the same month last year, marking a 24% year-over-year rise. This indicates a solid demand from buyers.

- Pending Sales: A leading indicator of next month’s sales data, pending sales surged 27% from last year, suggesting strong buyer interest and momentum that’s likely to carry forward.

- Active listings: In terms of supply, listings are the reservoir of options for buyers. October saw a 24% increase in new listings, with overall inventory levels 25% higher than a year ago.

- Median Sale Prices: The median closed sale price across the Northwest MLS rose 7%, from $625,000 last October to $671,000 this year. This growth reflects both increased demand and the wider range of active listings available to buyers, who responded to a summer decline in mortgage rates by stepping up purchase activity.

Overall, October’s data shows a market that is recalibrating toward a more balanced state, with robust buyer interest keeping momentum high.

A Closer Look at the Seattle Metro Area: King, Pierce, and Snohomish Counties

To get a deeper understanding of specific trends, let’s explore activity in the three counties comprising the Seattle metro area—King, Pierce, and Snohomish Counties.

- Sales Growth by County

King County: Residential closed sales rose an impressive 33% year-over-year. This area, including Seattle and Bellevue, saw a strong response from buyers.

Pierce County: Pierce County, which includes Tacoma, experienced a 26% increase in closed sales compared to last year.

Snohomish County: In Snohomish, home to cities like Everett, closed sales increased 20% year-over-year.

- Median Sale Prices by County

King County: The median sale price grew by 9%, reaching $960,000.

Pierce County: Pierce County’s median sale price rose 9%, up to $580,000.

Snohomish County: Snohomish saw the largest price growth, with an 11% increase, bringing the median price to $730,000.

- Pending Sales and Listings in the Seattle Metro

Pending sales continue to show strength across all three counties, with a notable 33% increase in King, 38% in Pierce, and 19% in Snohomish. These figures suggest strong buyer engagement and point to continued momentum.

The supply of active listings rose significantly, with increases of 25% in King County, 31% in Pierce, and 22% in Snohomish. The additional listings have provided buyers with more options, which is likely contributing to the increase in closed and pending sales.

What’s Next? A Preview of the Spring Market

This October report reveals signs of life returning to Washington’s local housing markets. Importantly, it’s a “proof of concept” that when mortgage rates dip closer to 6%, we see renewed energy and activity as people are ready to buy, sell, and move.

If rates continue their downward trend this winter, we could see even greater enthusiasm and market activity during the spring selling season.

If you have any questions, please reach out anytime: drew@windermere.com.

Buying a Home •

November 7, 2024

Renting vs. Buying: The Net Worth Gap You Need To See

Trying to decide between renting or buying a home?

One key factor that could help you choose is just how much homeownership can grow your net worth.

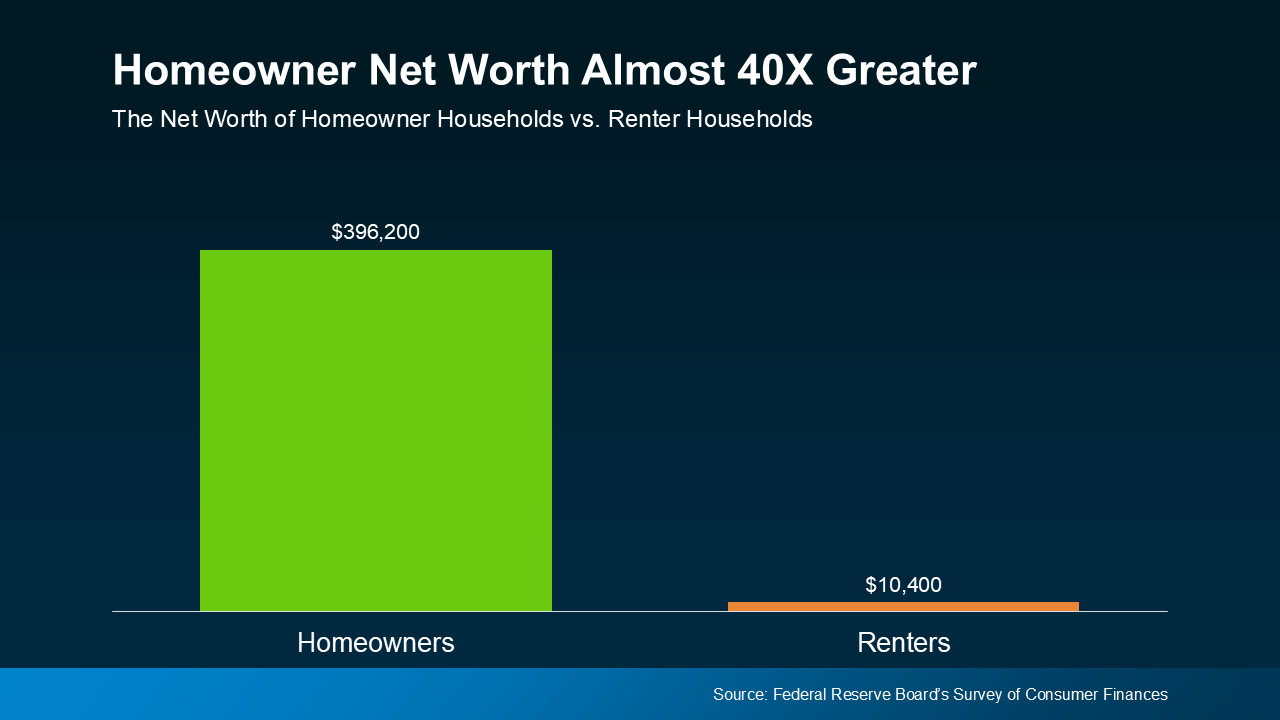

Every three years, the Federal Reserve Board shares a report called the Survey of Consumer Finances (SCF). It shows how much wealth homeowners and renters have – and the difference is significant.

On average, a homeowner’s net worth is nearly 40 times higher than a renter’s. Check out the graph below to see the difference for yourself:

Why Homeowner Wealth Is So High

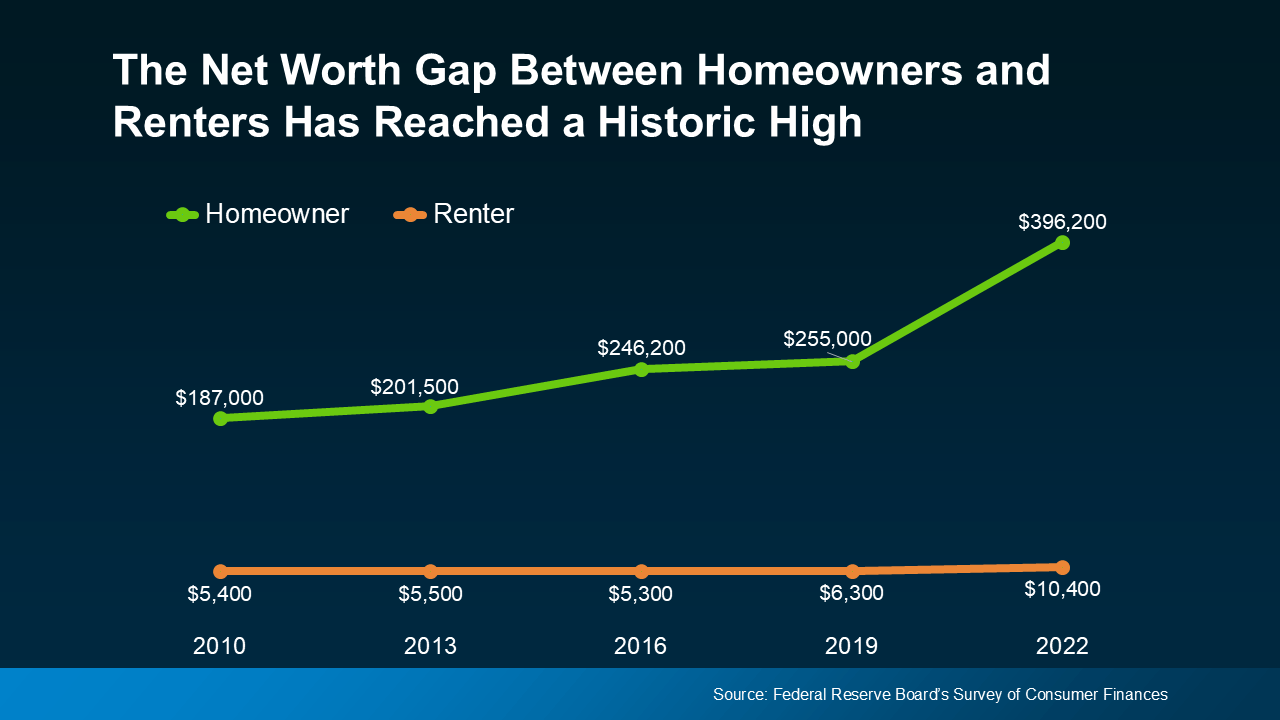

In the previous version of that report, the average homeowner’s net worth was about $255,000, while the average renter’s was just $6,300. That’s still a big gap. But in the most recent update, the spread got even bigger as homeowner wealth grew even more (see graph below):

As the SCF report says:

As the SCF report says:

“. . . the 2019-2022 growth in median net worth was the largest three-year increase over the history of the modern SCF, more than double the next-largest one on record.”

One big reason why homeowner wealth shot up is home equity.

Equity is the difference between your home’s value and what you owe on your mortgage. You gain equity by paying down your mortgage and when your home’s value goes up.

Over the past few years, home prices have gone up a lot. That’s because there weren’t enough available homes for all the people who wanted one. This supply-demand imbalance pushed home prices up – and that translated into faster equity gains and even more net worth for homeowners.

If you’re still torn between whether to rent or buy, here’s what you should know. While inventory has grown this year, in most places, there’s still not enough to go around. That’s why expert forecasts show prices are expected to go up again next year nationally. It’ll just be at a more moderate pace.

While that’s not the sky-high appreciation we saw during the pandemic, it still means potential equity gains for you if you buy now. As Ksenia Potapov, Economist at First American, explains:

“Despite the risk of volatility in the housing market, homeownership remains an important driver of wealth accumulation and the largest source of total wealth among most households.”

But prices and inventory are going to vary by area. So, give me call if you’re thinking of making a move. I can provide local trends and data in areas you’re interested in and work with you to find a path towards your home ownership hopes and goals.

So, if you’re not sure if you should rent or buy, keep in mind that if you can make the numbers work, owning a home can really grow your wealth over time.

Mortgage Rates •

November 7, 2024

This Week’s Fed Meeting: What to Expect

The Fed meets again this week to decide the next step with the Federal Funds Rate. So, let’s dig into how their decisions will impact the housing market.

First, the Federal Funds Rate is how much it costs banks to borrow from each other. Although that’s not the same as setting mortgage rates, mortgage rates can be influenced through this process.

If you’re thinking of buying or selling your home, here’s a quick rundown of what you need to know to help you anticipate what’ll happen next. The Fed’s decisions are guided by these three key economic indicators:

- The Direction of Inflation

- How Many Jobs the Economy Is Adding

- The Unemployment Rate

Let’s take a look at each one:

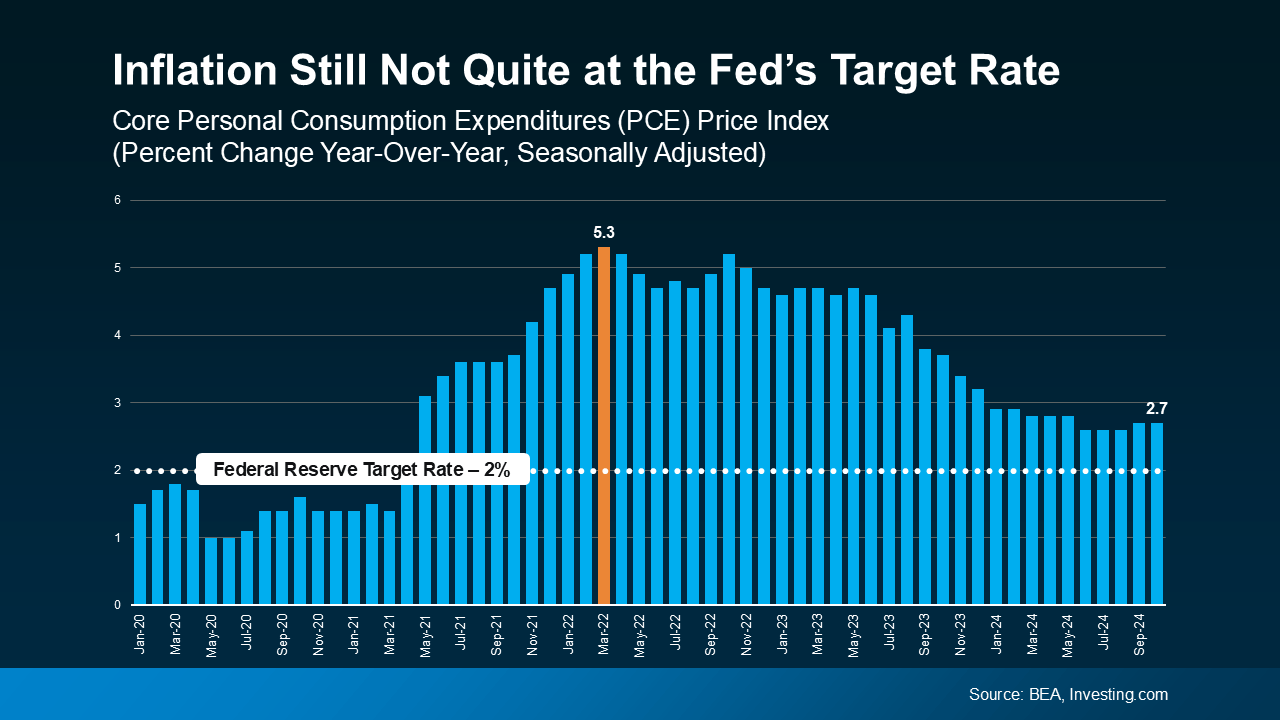

1. The Direction of Inflation

You’ve likely noticed prices for everyday goods and services seem to be climbing higher and higher.. That’s because of inflation – and the Fed wants to see that number come back down so it’s closer to their 2% target.

Right now, it’s still higher than that. But despite a little volatility, inflation has generally been moving in the right direction. It gradually came down over the past two years, and is holding fairly steady right now (see graph below):

The path of inflation – though still not at their target rate – is a big part of the reason why the Fed will likely lower the Fed Funds Rate again this week to make borrowing less expensive, while still ensuring the economy continues to grow.

The path of inflation – though still not at their target rate – is a big part of the reason why the Fed will likely lower the Fed Funds Rate again this week to make borrowing less expensive, while still ensuring the economy continues to grow.

2. How Many Jobs the Economy Is Adding

The Fed is also keeping an eye on how many new jobs are added to the economy each month. They want job growth to slow down a bit before they cut the Federal Funds Rate further. When fewer jobs are created, it shows the economy is still doing well, but gradually cooling off—exactly what they’re aiming for. And that’s what’s happening right now. Reuters says:

“Any doubts the Federal Reserve will go ahead with an interest-rate cut . . . fell away on Friday after a government report showed U.S. employers added fewer workers in October than in any month since December 2020.”

Employers are still hiring, but just not as many positions right now. This shows the job market is starting to slow down after running hot for a while, which is what the Fed wants to see.

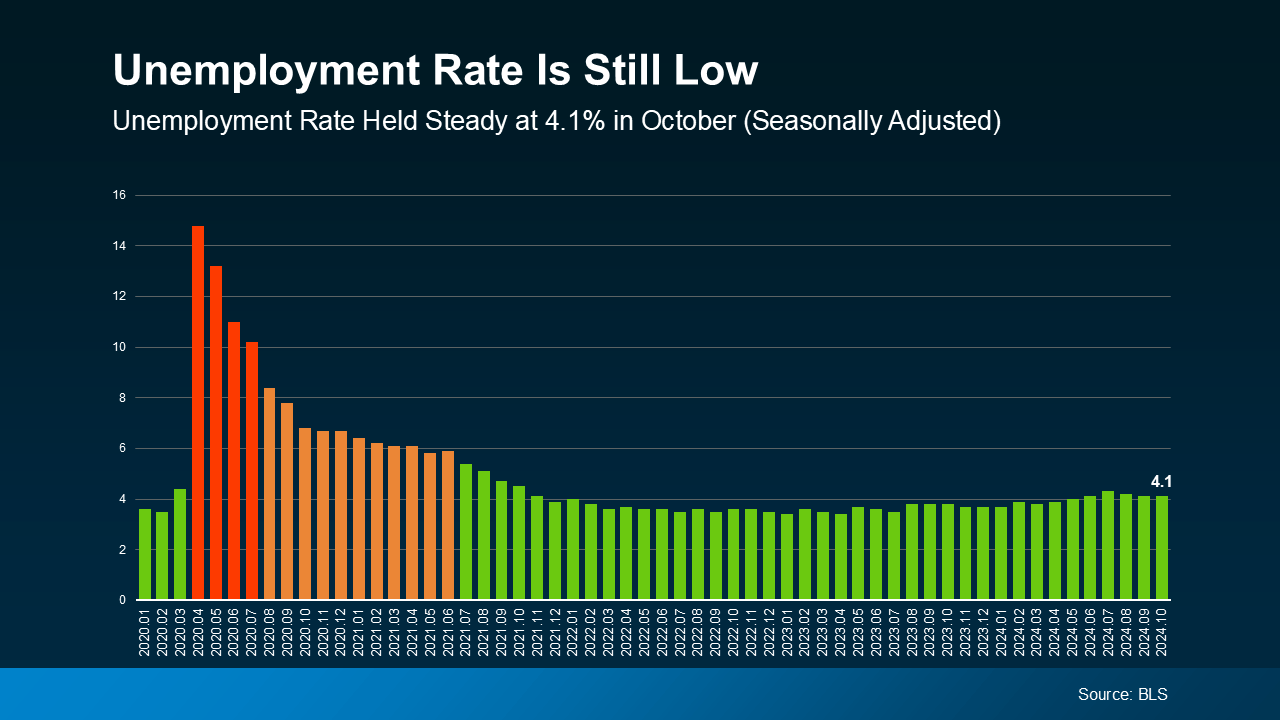

3. The Unemployment Rate

The unemployment rate shows the percentage of people who want jobs but can’t find them. A low unemployment rate means most people are working, which is great. However, it can push inflation higher because more people working means more spending—and that makes prices go up.

Many economists consider any unemployment rate below 5% to be as close to full employment as is realistically possible. In the most recent report, unemployment is sitting at 4.1% (see graph below):

Unemployment this low shows the labor market is still strong even as fewer jobs were added to the economy. That’s the balance the Fed is looking for.

Unemployment this low shows the labor market is still strong even as fewer jobs were added to the economy. That’s the balance the Fed is looking for.

What Does This Mean Going Forward?

Overall, the economy is headed in the direction the Fed wants to see – and that’s why experts say they will likely cut the Federal Funds Rate by a quarter of a percentage point this week, according to the CME FedWatch Tool.

If that expectation ends up being correct, that could pave the way for mortgage rates to come down too. But, it’ll take some time for them to fall. Remember, the Fed doesn’t determine mortgage rates. Forecasts show mortgage rates will ease more gradually over the course of the next year as long as these economic indicators continue to move in the right direction and the Fed can continue their Federal Funds rate cuts through 2025.

But a change in any one of the factors mentioned here could cause a shift in the market and in the Fed’s actions in the days and months ahead. So, brace for some volatility, and for mortgage rates to respond along the way. As Ralph McLaughlin, Senior Economist at Realtor.com, notes:

“The trajectory of rates over the coming months will be largely dependent on three key factors: (1) the performance of the labor market, (2) the outcome of the presidential election, and (3) any possible reemergence of inflationary pressure. While volatility has been the theme of mortgage rates over the past several months, we expect stability to reemerge towards the end of November and into early December.”

While the Fed’s actions play a part, economic data and market conditions are what really drive mortgage rates. At the moment, rates are expected to stabilize, with some possible downward movement, as we move through the rest of 2024.

Selling Your House •

October 28, 2024

Planning To Sell Your House in 2025? Start Prepping Now

If your goal is to sell your house in 2025, now’s the time to start prepping. Even though it might seem like there’s plenty of time between now and the new year, you should get a head start on any updates or repairs you want to make now. As Danielle Hale, Chief Economist at Realtor.com, says:

“ . . . now is the time to start thinking about what you need for your next home and then taking those steps to prepare to list . . . We have survey data that says 47 percent of sellers are taking longer than a month to get their home ready to sell, so getting them to start that process early can mean more flexibility.”

By starting your prep work early, you’ll give yourself plenty of time to get your house market-ready by the end of the year. But be sure to partner with a great agent before you get started, so you have expert insight into what repairs are worth it based on your local market.

Why Starting Early Is Key

To get the best price and sell quickly, it’s important that your home looks its best. And that means it’s up to you to make the necessary repairs, declutter, and even consider updates that could add value as part of getting your house ready to list.

By starting now, you can tackle things one task at a time. Whether it’s fixing that leaky faucet, refreshing your landscaping, or painting a room, getting an early start gives you the flexibility to do the job right and with as little stress as possible. Because, if you wait to knock items off your list later on, they could quickly stack up and get overwhelming. As Realtor.com explains:

“There are some important repairs to make before selling a house, so don’t be in too much of a hurry to get your home listed … if you move too fast, buyers see right through the fact that you skipped important home renovations. And this . . . might end up costing you time and money.”

What Should You Focus On?

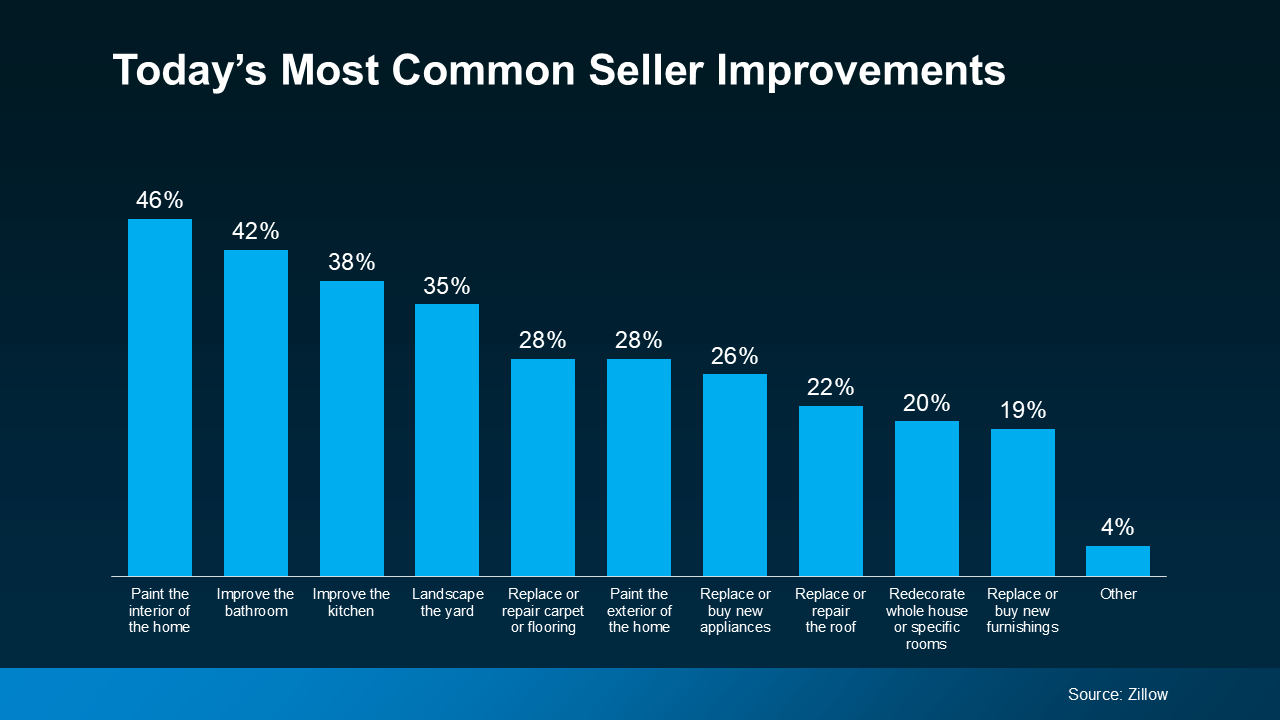

Feeling motivated to start chipping away at that to-do list, but not sure where to start? Here’s a look at the most common improvements other sellers are making today (see graph below):

The Importance of Working with a Local Agent

And while that data gives you a starting point, it shouldn’t be seen as a comprehensive list. What buyers want in your area may be different, and only a local agent will have this in-depth understanding.

For example, if homes in your area are selling quickly with updated kitchens, your agent might suggest focusing on minor kitchen improvements rather than spending money on other areas that won’t offer as much return. They’ll also help you figure out if tackling larger projects, such as replacing your roof or upgrading your HVAC system, is worth it based on other recently sold homes. As Point says:

“Not all renovations are created equal, and focusing on upgrades that offer the highest potential for increasing your home’s value is key.”

And remember, it’s not just big-ticket items that can have an impact. Your agent will also speak to some of the smaller details – like cleaning up your yard, adding fresh mulch, or painting your front door – to make a real difference in how buyers feel about your home. This type of expert eye is crucial to help your house sell fast and for top dollar.

So, if you’re thinking of selling your house next year, don’t wait until the last minute to get it ready. By getting a head start now, you can ensure everything is in place by the time the new year rolls around.

Need advice on what to tackle first? Let’s connect.

Buying a Home •

October 16, 2024

The Benefits of Using Your Equity To Make a Bigger Down Payment

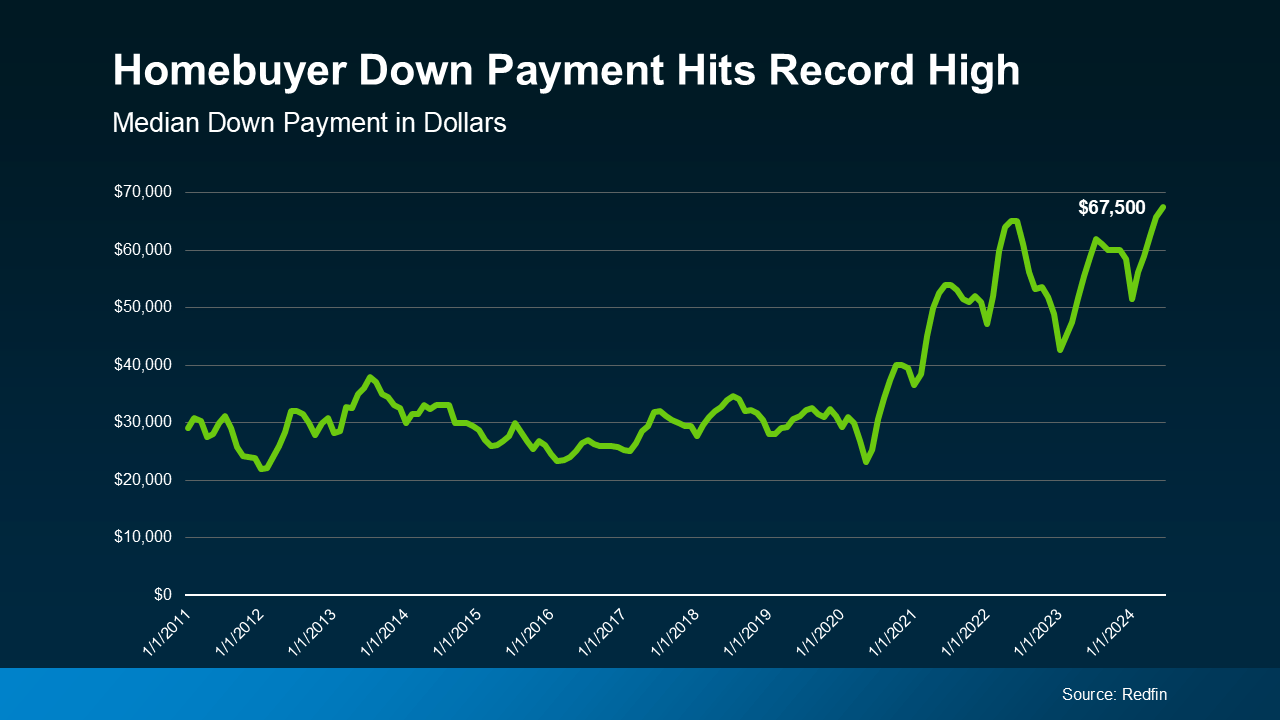

Did you know? Homeowners are often able to put more money down when they buy their next home. That’s because, once they sell, they can use the equity they have in their current house toward their next down payment. And it’s why as home equity reaches a new height, the median down payment has too.

According to the latest data from Redfin, the typical down payment for U.S. homebuyers is $67,500—that’s nearly 15% more than last year, and the highest on record (see graph below):

Here’s why equity makes this possible. Over the past five years, home prices have increased significantly, which has led to a big boost in equity for current homeowners like you. When you sell your house and move, you can take the equity that gives you and apply it toward a larger down payment on your new home. That’s a major opportunity, especially if you’ve had concerns about affordability.

Here’s why equity makes this possible. Over the past five years, home prices have increased significantly, which has led to a big boost in equity for current homeowners like you. When you sell your house and move, you can take the equity that gives you and apply it toward a larger down payment on your new home. That’s a major opportunity, especially if you’ve had concerns about affordability.

Now, it’s important to remember you don’t have to make a big down payment to buy your next home—there are loan programs that let you put as little as 3%, or even 0% down. But there’s a reason so many current homeowners are opting to put more money down. That’s because it comes with some serious perks.

Why a Bigger Down Payment Can Be a Game Changer

1. You’ll Borrow Less and Save More in the Long Run

When you use your equity to make a bigger down payment on your next home, you won’t have to borrow as much. And the less you borrow, the less you’ll pay in interest over the life of your loan. That’s money saved in your pocket for years to come.

2. You Could Get a Lower Mortgage Rate

Providing a larger down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage rate they’ll likely be willing to give you. And that amplifies your savings.

3. Your Monthly Payments Could Be Lower

A bigger down payment doesn’t just help you reduce how much you have to borrow—it also means your monthly mortgage payment may be smaller. That can make your next home more affordable and give you a bit more breathing room in your budget.

4. You Can Skip Private Mortgage Insurance (PMI)

If you can put down 20% or more, you can avoid Private Mortgage Insurance (PMI), which is an added cost many buyers have to pay if their down payment isn’t as large. Freddie Mac explains it like this:

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage. It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%.”

Avoiding PMI means you’ll have one less expense to worry about each month, which is a nice bonus.

So, down payments are at a record high, largely because recent equity gains are putting homeowners in a position to put more money down.

If you’re thinking about selling your current house and moving, let’s work together to figure out how much home equity you have right now, and how it can boost your buying power in today’s market.

Seasonal Home Maintenance •

October 14, 2024

6 Easy Ways to Protect Your Home from Rain Damage

I love rainy days. The sound of rain on the roof and windows usually provides me with a peaceful, relaxed feeling. I remember one time, though, when the sound of raindrops sounded more like alarm bells going off than a soft, cozy pitter-patter.

Years ago, when my wife and I were new homeowners (and before I was a realtor), I was at the office on a rainy day in January. My phone rang and I picked it up to hear my wife’s stressed voice telling me I needed to come home asap. The basement carpet was soaking wet.

I rushed home. My wife and I lifted the carpet, put sandbags down, and did everything we could to stop our things and our home from complete catastrophe.

That week felt like a crash course in homeownership. We replaced the carpet, installed a sump pump, and gained a wealth of knowledge about safeguarding our home from the devastating effects of water damage.

As homeowners in the Pacific Northwest, it’s essential to protect your valuable home from water damage. Over many years of working in real estate, I’ve seen water damage affect all parts of people’s homes, ranging from minor to catastrophic. I don’t want that to happen to you.

If I’m your realtor, you can be sure I’ll help you spot potential issues – raindrops on your roof should lull you to sleep, not send you into a middle-of-the-night scramble to stop a disaster.

Here are 6 key things you can do to prevent water damage:

- Keep your gutters and downspouts clear.

Make sure they’re free of debris so water flows freely and away from your home. You’ll prevent water from accumulating on your roof and causing leaks and damage.

- Inspect your roof regularly

You can look for missing or damaging shingles, cracking, and other signs of wear and tear. If you notice anything, have it repaired as soon as possible so water won’t find its way into your house.

- Seal your windows and doors.

I’ve learned this one the hard way too. Take the time to seal around windows and doors, so you can prevent water from leaking in and damaging your interior walls and rooms.

- Check your grading and drainage.

Where is the water running once it hits the ground? If your yard doesn’t slope away from your home, you can create ways for the water to drain away from the house so it doesn’t pool, causing flooding and/or foundation damage.

- Check your sump pump.

If you have a sump pump, make sure it’s in working order and not blocked by debris.

- Create a disaster plan.

It’s always a good idea to be prepped for emergencies. Having sandbags and tarps on hand can help in the case of flooding. Make sure you and your family know what to do in case of flooding and severe weather, and know how to shut off your utilities in case of an emergency.