Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Real Estate News •

October 8, 2024

Seattle Real Estate: Numbers You Need to Know Now

In today’s economy, understanding the latest numbers can give us valuable insights into where things are headed. Here are three key figures from the latest jobs report and their implications for the market.

The numbers and commentary below come directly from Windermere’s Principal Economist Jeff Tucker’s recent video that you can watch here.

254,000

That’s the number of net jobs added in September, according to the latest jobs report released on Friday, October 4th. This is a strong report, far exceeding the expected 145,000 jobs forecasted. Additionally, payroll counts for July and August were revised upward by 72,000 jobs combined. Altogether, this makes September the best month for job gains since March of this year, bucking the trend of a cooling labor market seen over the summer months.

4.1%

This is the unemployment rate for September, down slightly from 4.2% in August and 4.3% in July. The combination of falling unemployment and rebounding job growth points to an economy that’s in much better shape than it was over the summer. In other words, concerns about a looming recession are easing, which leads us to our final number…

6.5%

This is the latest 30-year mortgage rate, which jumped by about a quarter point following the strong jobs report on Friday, October 4th. While this was a significant one-day increase, it’s important to put it in context. Rates are still roughly where they were in August, and they remain down almost a full percentage point from their levels in April and May of this year. Compared to this time last year, mortgage rates have dropped by more than a point. However, this is a reminder that rate cuts won’t follow a smooth, predictable pattern—instead, we should expect more of a “zigzag” when it comes to mortgage rates.

Any questions? Feel free to contact me anytime with your real estate questions and needs.

Real Estate Agents •

October 8, 2024

4 Myths About Real Estate Agents—Debunked!

When it’s time to buy or sell a home, one of the most important decisions you’ll make is who you’ll work with as your agent. That choice will have an impact on your entire experience and how smoothly it goes.

And, you’ve probably heard a few things about real estate agents—some of them are spot on, but others? Not so much. Let’s take a minute to break down four common myths about real estate agents and why they simply don’t hold up—especially if you’re working with a local expert like me!

Myth #1: All Real Estate Agents Are the Same

This myth couldn’t be further from the truth. Real estate agents differ in experience, local knowledge, and approach. Working with an agent who truly knows the ins and outs of your local market makes a huge difference. It’s not just about finding you a home, it’s about finding the right home that fits your needs and has solid resale value down the road. When you choose an agent, you want someone who’s in tune with the market and who will take the time to understand exactly what you’re looking for.

Myth #2: You Can Save Money by Not Using an Agent

The idea that cutting out an agent will save you money might seem appealing, but in reality, it could cost you more. Without an agent, you’re navigating a complex process solo—negotiating, pricing, handling inspections, and more. A skilled agent not only guides you through these steps but can also help you avoid costly mistakes, like overpaying for a home or underpricing one you’re selling. Plus, agents are experts at negotiating the best possible deal, which often results in savings you wouldn’t have achieved on your own.

That’s why U.S. News Real Estate says:

“When it comes to buying or selling your home, hiring a professional to guide you through the process can save you money and headaches. It pays to have someone on your side who’s well-versed in the nuances of the market and can help ensure you get the best possible deal.”

Myth #3: Agents Will Push You To Spend More

A common misconception is that agents push buyers to spend more so they can earn a bigger commission. As a professional, I can assure you that this is not how I—or any good agent—operate. My goal is to help you find a home that fits your needs and your budget. I want to make sure you’re comfortable with your investment, and that means sticking to what works for you financially. Whether it’s your first home or your dream home, the focus is always on what’s best for you, not the price tag.

Myth #4: Market Conditions Are the Same Everywhere, So Why Do I Need a Pro?

Every market is different! Conditions that apply in one city, or even one neighborhood, may not apply in another. That’s why working with a local expert is key. I know the ins and outs of our market, from pricing trends to neighborhood amenities, and I keep my finger on the pulse of what’s happening. That knowledge helps me guide you toward properties that are not only a good fit for today but will also offer good resale value in the future.

At the end of the day, real estate is about so much more than just buying or selling a home. It’s about finding the right property for your life, your budget, and your long-term goals. As your local agent, I’m here to take the time necessary to make sure you get exactly what you’re looking for. If you’re ready to make a move or just have some questions, I’d love to help you navigate the process!

Selling Your House •

October 8, 2024

Why Now’s Not the Time To Take Your House Off the Market

Has your house been sitting on the market longer than expected? If so, you’re bound to be frustrated by now. Maybe you’re even thinking it’s time to pull the listing and wait to see what 2025 brings. But what you may not realize is, the decision to hold off could actually cost you. Here’s a look at why staying the course could be the smarter move.

Other Sellers Are Pulling Back. Should You Hold Off Too?

According to recent data from Altos Research, the number of withdrawals is increasing – that means more sellers are opting to pull their listings off the market right now. And this isn’t unusual for this time of the year.

In the housing market, there are seasonal ebbs and flows. Inventory levels typically start to drop off a bit headed into the fall season as some sellers delay their plans until the new year. As Mike Simonsen, Founder of Altos Research, explains:

“. . . we’re seeing a more normal seasonal pattern now with inventory beginning to decline. We’re also seeing more home sellers withdrawing their listings to try again next year. In fact, for every two sales, there is another listing withdrawn from the market.”

But is that a smart move? While it might seem like a good idea to pull your listing too, here’s why that approach may not pay off this year.

Today’s Buyers Are Serious and Ready To Act

The biggest reason to stick with your plan to sell now is that the buyers who are looking at this time of year are serious about making a purchase.

They’ve been sitting on the sidelines for a while waiting for affordability to improve. And now that mortgage rates are down from their recent peak, they’re ready to make their move. Mortgage applications are rising – and that’s a leading indicator that buyers are preparing to jump back in. And since they’ve already put their needs on the back burner for so long, they’re even more eager than buyers usually are at this time of year.

These aren’t window shoppers. They’re highly motivated buyers who want to move fast – and that’s the kind of buyer you want to work with. As Freddie Mac says:

“During the fall months, serious homebuyers are eager to settle in to a new home before the holiday season ramps up and the winter weather begins.”

By keeping your home on the market, you increase the chances of attracting people who are truly ready to make a purchase.

So, while some sellers are choosing to take their homes off the market, this may not be the best move. With serious buyers eager to purchase, this is a great time to sell your house. Let’s connect to make sure we’ve got a strategy in place to make it happen.

Buying a Home •

October 7, 2024

Should I buy now or wait?

If you’re wondering if you should buy now or wait, here’s what you need to know. If you wait for rates to drop more, you’ll have to deal with more competition and higher prices as additional buyers jump back in. But if you buy now, you’d get ahead of that and have the chance to start building equity. Should you buy now or wait? Let’s talk through it together, so you can make your best decision.

Buying a Home •

October 7, 2024

This Is the Sweet Spot Homebuyers Have Been Waiting For

After months of sitting on the sidelines, many homebuyers who were priced out by high mortgage rates and affordability challenges finally have an opportunity to make their move. With rates trending down, today’s market is a sweet spot for buyers—and it’s one that may not last long.

So, if you’ve put your own move on the back burner, here’s why maybe you shouldn’t delay your plans any longer.

As you weigh your options and decide if you should buy now or wait, ask yourself this: What do you think everyone else is going to do?

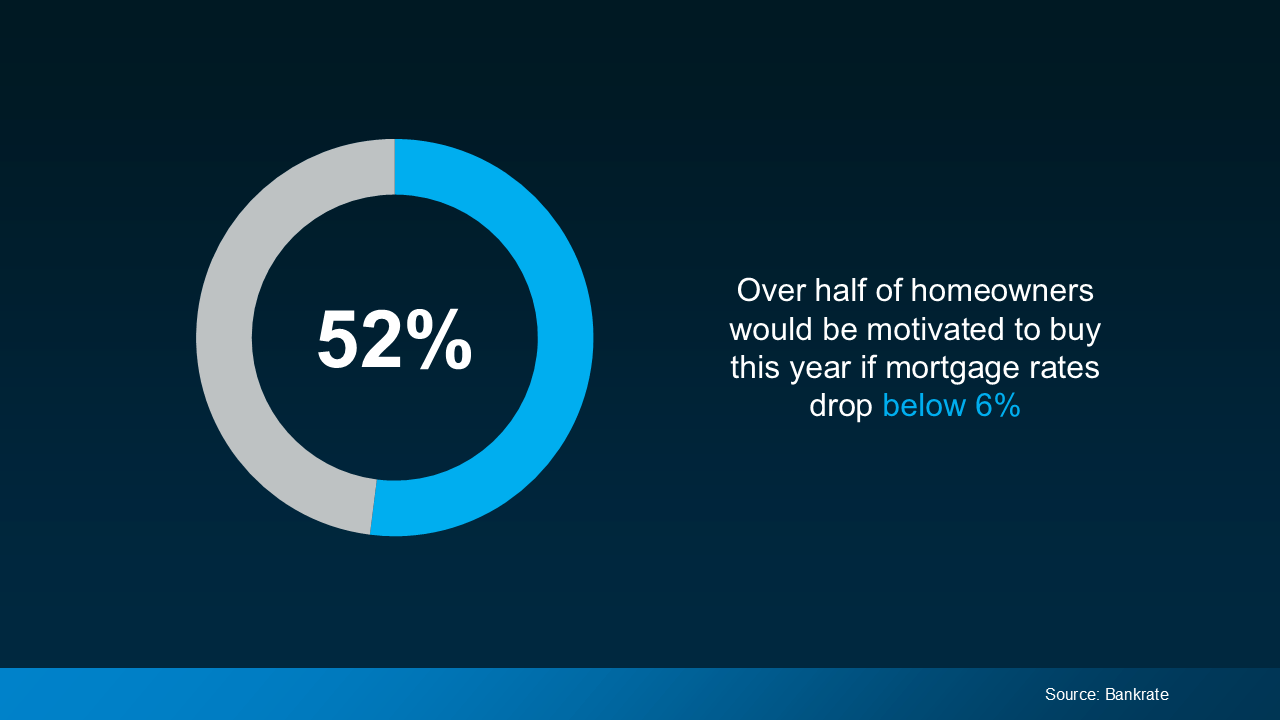

The truth is, if mortgage rates continue to ease, as experts project, more buyers will jump back into the market. A survey from Bankrate shows over half of homeowners would be motivated to buy this year if rates drop below 6% (see graph below):

With rates already in the low 6% range, we’re not terribly far off from hitting that threshold. The bottom line is, that when they drop into the 5s, the number of buyers in the market is going to go up – and that means more competition for you.

With rates already in the low 6% range, we’re not terribly far off from hitting that threshold. The bottom line is, that when they drop into the 5s, the number of buyers in the market is going to go up – and that means more competition for you.

That increased demand will likely push home prices up, which could potentially take away from some of the benefits you’d gain from a slightly lower interest rate. As Nadia Evangelou, Senior Economist and Director of Real Estate Research at the National Association of Realtors (NAR), explains:

“The downside of increased demand is that it puts upward pressure on home prices as multiple buyers compete for a limited number of homes. In markets with ongoing housing shortages, this price increase can offset some of the affordability gains from lower mortgage rates.”

So, while waiting to buy may seem like a smart move, it could backfire if rising prices outpace your savings from slightly lower rates.

What This Means for You

Right now, you’ve got the chance to get ahead of all of that. Today’s market is a buyer sweet spot. Why? Because a lot of other buyers are waiting – which means not as many people are actively looking for homes. That means less competition for you.

At the same time, affordability has already improved quite a bit. Recent easing in mortgage rates has made homeownership more accessible. As Mike Simonsen, Founder of Altos Research, says:

“Mortgage payments on the typical-price home are 7% lower than last year and are 13% lower than the peak in May 2024.”

And while the supply of homes for sale is still low, it’s also higher than it’s been in years. According to Ralph McLaughlin, Senior Economist at Realtor.com:

“The number of homes actively for sale continues to be elevated compared with last year, growing by 35.8%, a 10th straight month of growth, and now sits at the highest since May 2020.”

This means you now have more options to choose from than you’ve had in quite a while.

With fewer buyers in the market, improving affordability, and more homes to choose from, you have the chance to find the right one before the competition heats up.

Why Waiting Could Cost You

If you’re waiting for the perfect time to buy, it’s important to understand that timing the market is nearly impossible. The longer you wait, the higher the risk that market conditions will shift—and not necessarily in your favor. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“It’s one of those things where you should be careful what you wish for. A further drop in mortgage rates could bring a surge of demand that makes it tougher to actually buy a house.”

Don’t wait until you have to deal with more competition and higher prices – you already have the chance to buy a home while we’re in the sweet spot today. Let’s connect to make sure you’re taking advantage of it.

Affordability •

October 7, 2024

The Top 3 Reasons Affordability is Improving

Affordability is based on three key factors: mortgage rates, home prices, and wages. And today, it’s improving quickly as rates come down, prices level off, and wages climb. If you put your search on pause because it was too expensive to buy, let’s talk about why now may be the perfect time to jump back in.

Buying a Home •

October 7, 2024

Now’s the Time To Upgrade to Your Dream Home

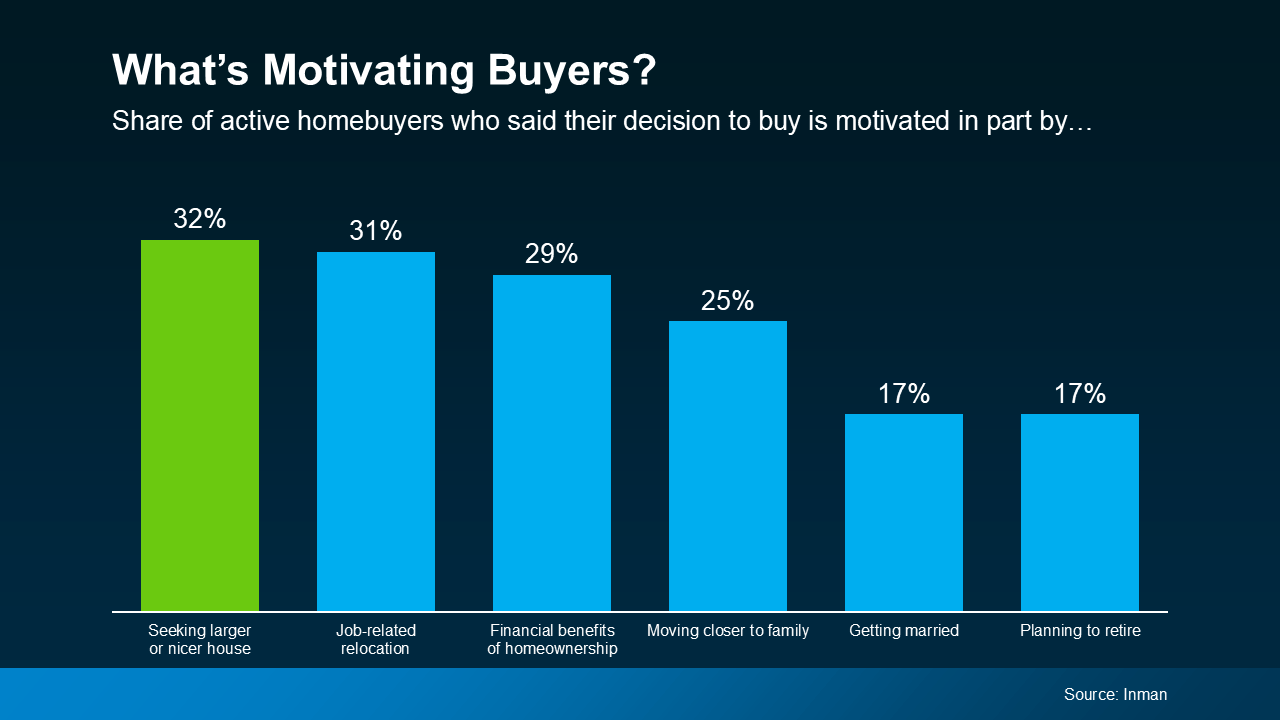

If you’ve been wanting to sell your house and move up to a bigger or nicer home, you’re not alone. A recent Inman survey reveals the top motivator for today’s homebuyers is the desire for more space or an upgraded home (see graph below):

But there’s also a good chance you, like many other people, have been holding off on that goal because of recent market challenges.

But there’s also a good chance you, like many other people, have been holding off on that goal because of recent market challenges.

It makes sense – when you’re planning an upgrade that could increase your monthly housing costs, affordability has a huge impact on when you make your move. But there’s good news: now’s actually a great time to make that move happen. Here’s why.

You Have a Lot of Equity To Leverage

One of the key benefits in today’s market is the amount of equity you’ve likely built up in your current house over the years. Even with recent shifts in the housing market, national home prices have steadily grown, adding to the equity homeowners have today. Selma Hepp, Chief Economist at CoreLogic, explains it well:

“Persistent home price growth has continued to fuel home equity gains for existing homeowners who now average about $315,000 in equity and almost $129,000 more than at the onset of the pandemic.”

What does that mean for you? If you’ve been in your home for a few years, you’re probably sitting on a significant amount of equity. You can put that toward the down payment on your next home, helping keep the amount you borrow within a comfortable range.

This can make upgrading more achievable than you might think. If you’re curious how much you’ve built up over the years, ask your real estate agent for a professional equity assessment.

Mortgage Rates Have Fallen, Boosting Your Purchasing Power

And there’s another big reason why now’s a great time to make your move: mortgage rates are trending down. Lower rates can help make your future monthly payments more manageable, and they also increase your purchasing power. As Nadia Evangelou, Senior Economist and Director of Real Estate Research at the National Association of Realtors (NAR), points out:

“When mortgage rates fall, the interest portion of monthly payments decreases, which lowers the total payment. This makes it easier for more borrowers to . . . qualify for mortgages that may have been unaffordable at higher rates.”

That gives you more flexibility when shopping for homes and may allow you to afford a house at a price point that was previously out of reach. A trusted lender can work with you to figure out the best plan for your budget.

If you’re ready to sell your current home and find the bigger, nicer home you’ve been dreaming of, don’t wait. Your equity, paired with lower mortgage rates, puts you in a great position to make that move today.

To make the best decisions and get the most out of your current market advantage, let’s connect so you have an expert guide through every step of the homebuying process.

Buying a Home •

September 24, 2024

The Down Payment Assistance You Didn’t Know About

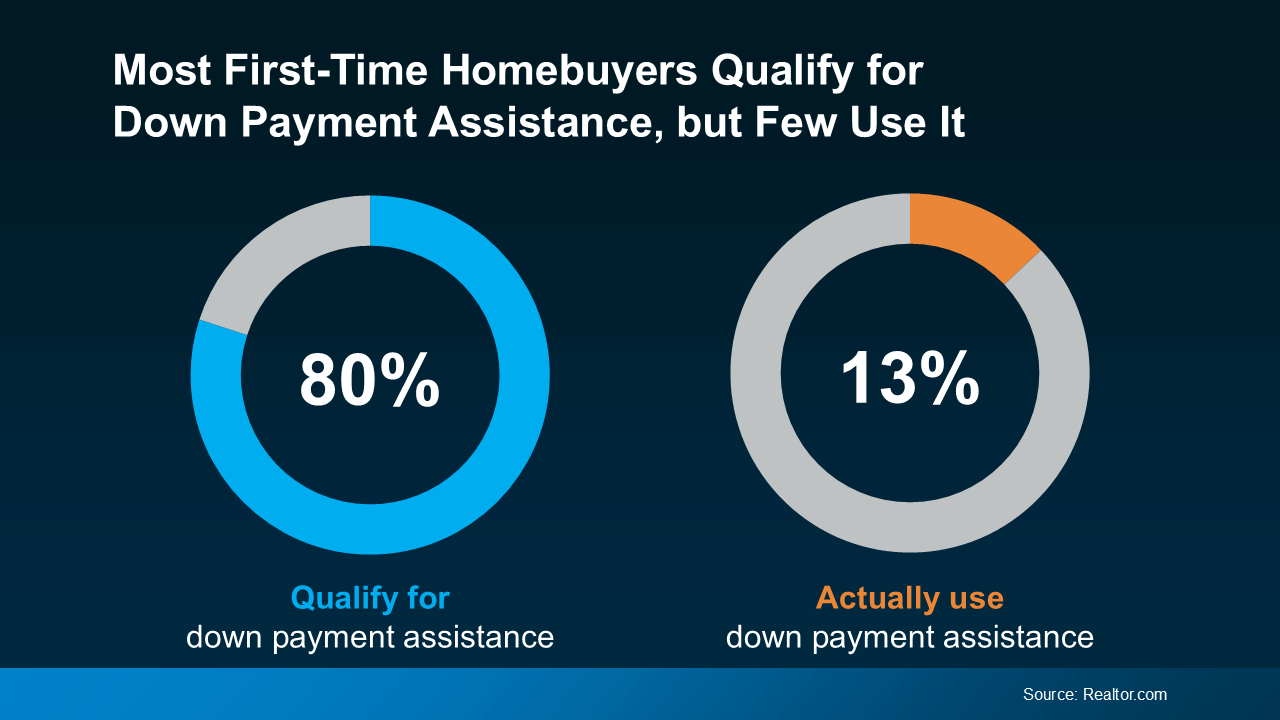

Believe it or not, almost 80% of first-time homebuyers qualify for down payment assistance, but only 13% actually use it. And if you’re hoping to buy a home, this is a mission-critical gap to close – fast (see graph below):

Here’s what you need to know to make the most of your down payment in today’s housing market.

Here’s what you need to know to make the most of your down payment in today’s housing market.

Amplify Your Down Payment Potential

For first-time buyers, the name of the game with down payments is making sure you’re taking advantage of all the resources out there designed to help you. And a bunch of them can get you to your goal faster than you may have thought possible.

For example, there are loan options that require as little as 3% down, or even 0% for certain qualified borrowers, like Veterans. And let’s not forget down payment assistance, like grants and other opportunities, that help you cover the upfront cost of your down payment.

If you’re interested in exploring those options and what you may be able to use to your advantage, connect with a trusted lender. Because if you don’t at least see what’s available, you could be leaving money on the table and missing your chance at buying a home. These resources can boost your down payment. And a higher down payment could help lower your eventual monthly mortgage payment, and even avoid or reduce your fees like private mortgage insurance.

Don’t Let News Headlines About Down Payments Scare You

There’s one more thing to address. News coverage has been talking about how the typical down payment is rising. A report from Redfin states:

“The typical down payment for U.S. homebuyers hit a record high of $67,500 in June, up 14.8% from $58,788 a year earlier . . . This was the 12th consecutive month the median down payment rose year over year.”

But don’t let those high dollars scare you. Just because the average down payment is rising doesn’t mean down payment requirements are going up. That’s a key piece of the puzzle to understand. It’s really just because people are choosing to put more down to try to offset higher mortgage rates, and current homeowners who are putting their equity to work are using that to increase their down payment on their next home. As HousingWire explains:

“. . . buyers are putting down a higher percentage of the purchase price to lower their monthly mortgage payment. And buyers also had more equity from their home sales, which gives them more cushion.”

Let’s break those two reasons down a bit:

1. A bigger down payment helps lower your monthly mortgage payment. Affordability has been a challenge for many buyers recently, which is why those who have the ability to make a bigger down payment are going to do so in an effort to lower their future housing costs.

2. Buyers who already own a home have a record amount of equity to leverage. Someone who bought a home a few years ago has gained a significant amount of value in their house, thanks to home price appreciation. These people can put down much more than the average first-time buyer who hasn’t owned a home yet.

What’s the best thing to do? Talk with a trusted lender about your options. They’ll help you figure out where you stand today and how to access the resources you may qualify for. Because help is out there, you just need to work with a pro to take advantage of it.

Buying a Home •

September 16, 2024

The Best Time To Buy a Home This Year

A shift is underway in the housing market this season. And if you’ve been sitting on the sidelines waiting for the right moment to jump back into your homebuying search, this is a great time to do it. That’s because the best week to buy a home this year is just around the corner.

The experts at Realtor.com study seasonal trends to figure out the ideal week for homebuyers:

“Nationally, the best time to buy in 2024 is the week of Sept. 29–Oct. 5. This week historically has shown the best balance of market conditions that favor buyers. Inventory tends to be high, prices are below peak levels, demand is waning, and the pace of the market slows to a more manageable speed.”

In addition to the historical trends and typical seasonality that Realtor.com looks at, there are also clear indicators in today’s market data that you’ll see better conditions right now than you would have over the last few years.

Mortgage rates just hit their lowest point in 19 months, and that goes a long way to help with your purchasing power and affordability. Andy Walden with Intercontinental Exchange Inc. (ICE) points out:

“Recent easing in mortgage rates brought some much-sought relief to prospective homebuyers. Along with a general cooling in home price growth, rates falling below 6.5 percent made August the most affordable month for housing since February.”

And Ralph McLaughlin, Senior Economist at Realtor.com, explains that it’s not just rates that have improved – inventory has too:

“The number of homes actively for sale continues to be elevated compared with last year, growing by 35.8%, a 10th straight month of growth, and now sits at the highest since May 2020.”

That should give you more options. At the same time, sellers now have to compete with each other for your attention. That means they’ll be more likely to negotiate because they know their house will sit on the market longer if they don’t. As Zillow says:

“Buyers waiting on the sidelines could find that early fall presents a ‘sweet spot,’ where there’s less competition from other buyers, more motivated sellers and lower interest rates to finance their purchases.”

If you want to make sure you’re ready to take advantage of this sweet spot, let’s connect and start the prep work now. Maybe it’s time to get off the sidelines and into the action.