Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Selling Your House •

September 13, 2024

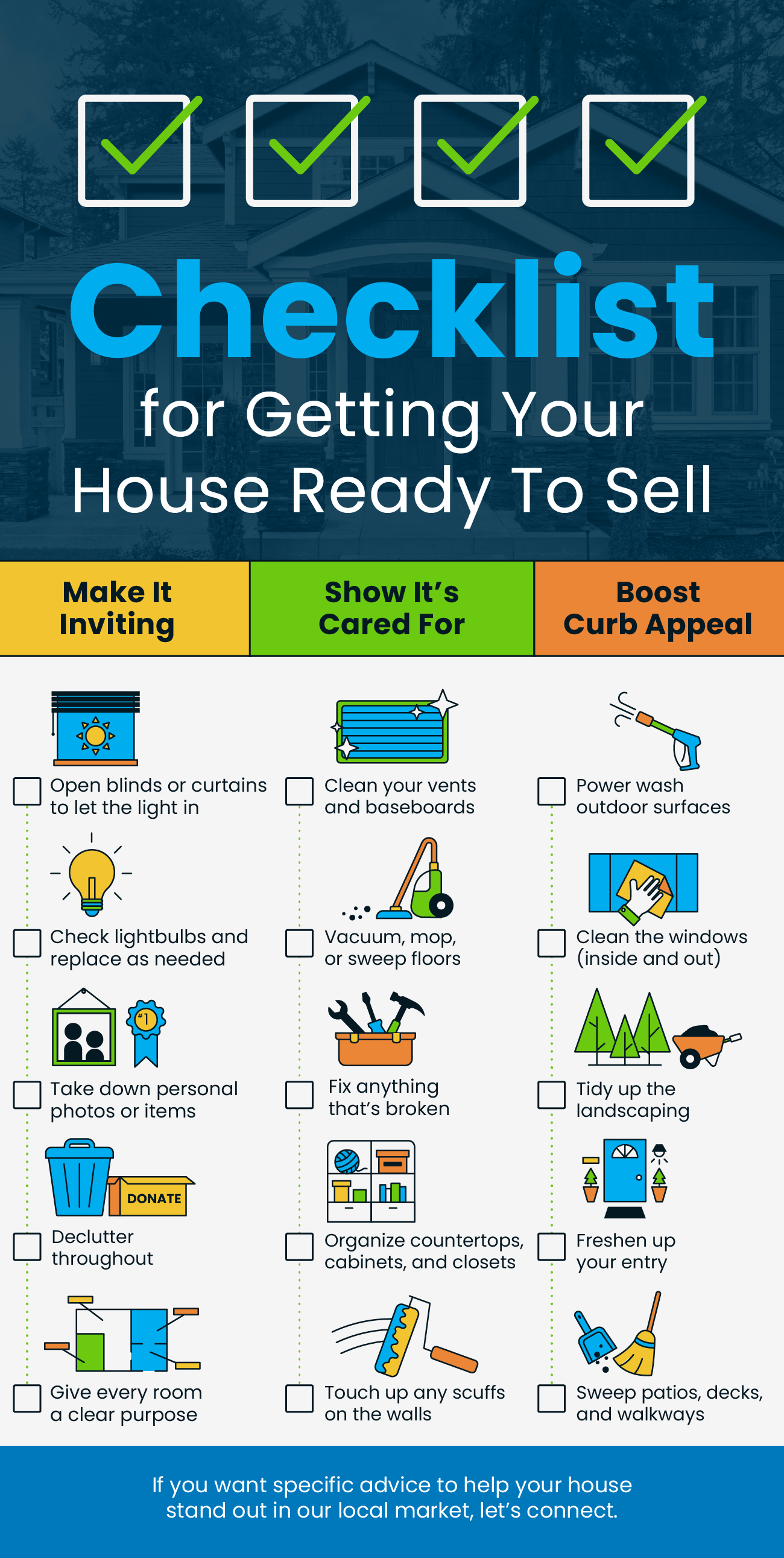

Checklist for Getting Your House Ready To Sell

Some Highlights

- Getting your house ready to sell? Here are a few tips on what you may want to do to prepare.

- Focus on making it inviting, showing it’s cared for, and boosting your curb appeal.

- If you want specific advice to help your house stand out in our local market, let’s connect.

Seasonal Home Maintenance •

September 12, 2024

5 Tips for Creating a Cozy, Autumn Oasis at Home

Fall is a fantastic time to showcase your home because it offers unique opportunities to create warmth, coziness, and charm. If you’re planning to sell this fall, I highly recommend using a professional stager. Staging is often a key ingredient to a successful selling strategy.

However, even if you’re not selling, it’s fun to use some expert tips and ideas to boost your home’s cozy vibes and fall feels. Here are five expert staging tips for making your home extra homey this fall:

1. Enhance Lighting

As daylight becomes more scarce, make sure to maximize your home’s natural light. Clean windows and replace outdated curtains with sheer or light-colored options. Consider adding strategically placed mirrors to reflect light and brighten spaces.

If your home is lacking in natural light, look for places where an added light or lamp might brighten the room. White, light, and neutral paints are a key part of staging your home and they can help lift the brightness of your home.

Finally, don’t forget outside lights. Make sure your exterior lights are on and paths are lighted if needed. Exterior lights are a great way to enhance curb appeal, welcome guests, and provide extra safety for walking. You can make your home glow with autumnal charm.

2. Cozy up with Textiles

Nothing says “welcome home” like soft, cozy textiles. Professional stagers might use plush throw blankets, seasonal accent pillows, and area rugs in warm, autumnal colors to create a sense of comfort in your living spaces.

Tasteful, fall touches can help accentuate a home’s ambience. A well-placed autumn wreath on the front door, a decorative bowl of apples or gourds on the dining table, and a few pumpkins on the porch are nice seasonal accents.

3. Fireside Comforts

If your home has a fireplace, arrange seating around it. And, of course, lighting or turning on the fire is the perfect way to create instant warmth.

4. Curb Appeal:

Along with exterior lights, it’s also important to keep the outside of your home fresh and clean to emphasize your yard’s natural autumn beauty. Rake leaves, clean out gutters, and add some seasonal potted plants, like mums, to boost curb appeal.

PNW residents love their outdoor spaces, even in the fall. Ensure that decks and patios are clean and inviting. Stage them with cozy seating, blankets, and perhaps some café lights and/or a fire pit to showcase the potential for year-round enjoyment.

5. It Makes Scents

Finally, stagers often suggest appealing to the senses with the comforting scents of autumn. Consider using subtle, pleasant, scented candles, essential oil diffusers, or potpourri with fall scents like apple cinnamon, pumpkin spice, or warm vanilla.

With these fall staging tips, you can already envision yourself snuggled up with a book by the fire or sipping hot cider on the patio.

If you’re thinking of selling this fall and need advice or assistance, please reach out to me. I’m here to help you make your property stand out in the Seattle area real estate market this fall.

Selling Your House •

September 12, 2024

Should You Sell Now? The Lifestyle Factors That Could Tip the Scale

Are you on the fence about whether to sell your house now or hold off? It’s a common dilemma, but here’s a key point to consider: your lifestyle might be the biggest factor in your decision. While financial aspects are important, sometimes the personal motivations for moving are reason enough to make the leap sooner rather than later.

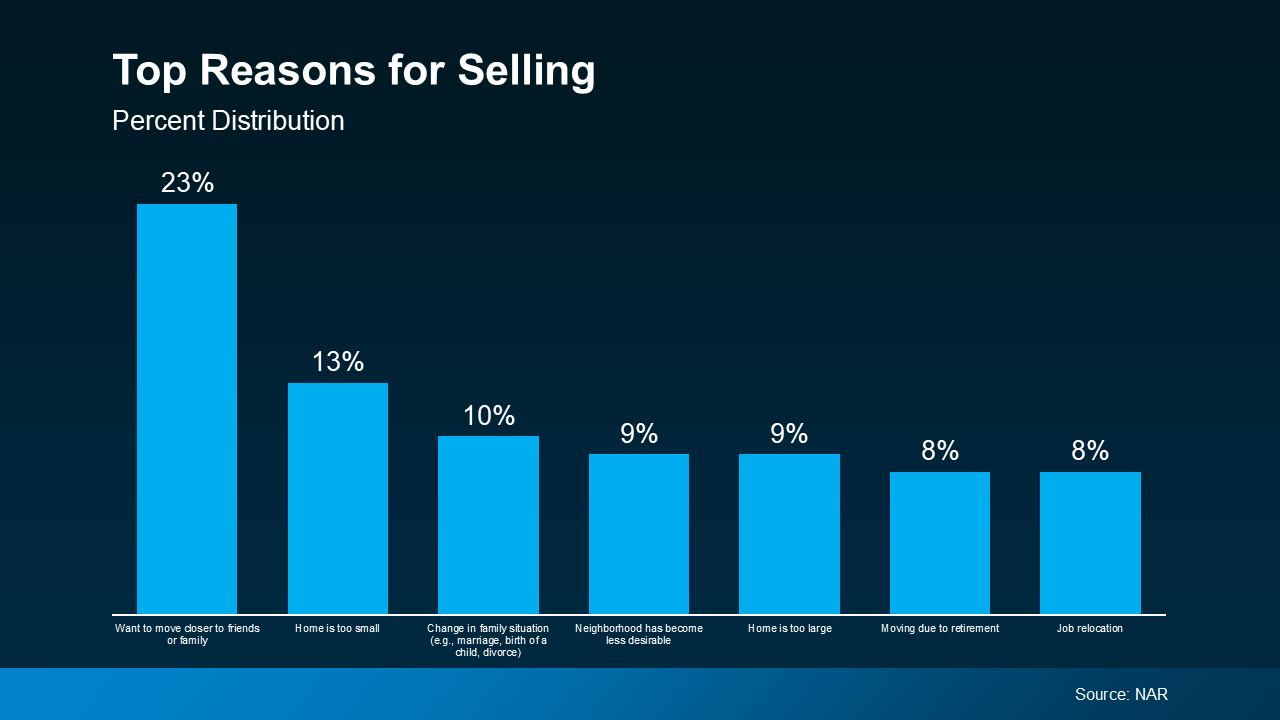

An annual report from the National Association of Realtors (NAR) offers insight into why homeowners like you chose to sell. All of the top reasons are related to life changes. As the graph below highlights:

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

If you, like the homeowners in this report, find yourself needing features, space, or amenities your current home just can’t provide, it may be time to consider talking to a real estate agent about selling your house. Your needs matter. That agent will walk you through your options and what you can expect from today’s market, so you can make a confident decision based on what matters most to you and your loved ones.

Your agent will also be able to help you understand how much equity you have and how it can make moving to meet your changing needs that much easier. As Danielle Hale, Chief Economist at Realtor.com, explains:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

Your lifestyle needs may be enough to motivate you to make a change. If you want help weighing the pros and cons of selling your house, let’s chat!

Mortgage Rates •

September 12, 2024

How the Federal Reserve’s Next Move Could Impact the Housing Market

Now that it’s September, all eyes are on the Federal Reserve (the Fed). The overwhelming expectation is that they’ll cut the Federal Funds Rate at their upcoming meeting, driven primarily by recent signs that inflation is cooling, and the job market is slowing down. Mark Zandi, Chief Economist at Moody’s Analytics, said:

“They’re ready to cut, just as long as we don’t get an inflation surprise between now and September, which we won’t.”

But what does this mean for the housing market, and more importantly, for you as a potential homebuyer or seller?

Why a Federal Funds Rate Cut Matters

The Federal Funds Rate is one of the key factors that influences mortgage rates – things like the economy, geopolitical uncertainty, and more also have an impact.

When the Fed cuts the Federal Funds Rate, it signals what’s happening in the broader economy, and mortgage rates tend to respond. While a single rate cut might not lead to a dramatic drop in mortgage rates, it could contribute to the gradual decline that’s already happening.

As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), points out:

“Once the Fed kicks off a rate-cutting cycle, we do expect that mortgage rates will move somewhat lower.”

And any upcoming Federal Funds Rate cut likely won’t be a one-time event. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Generally, the rate-cutting cycle is not one-and-done. Six to eight rounds of rate cuts all through 2025 look likely.”

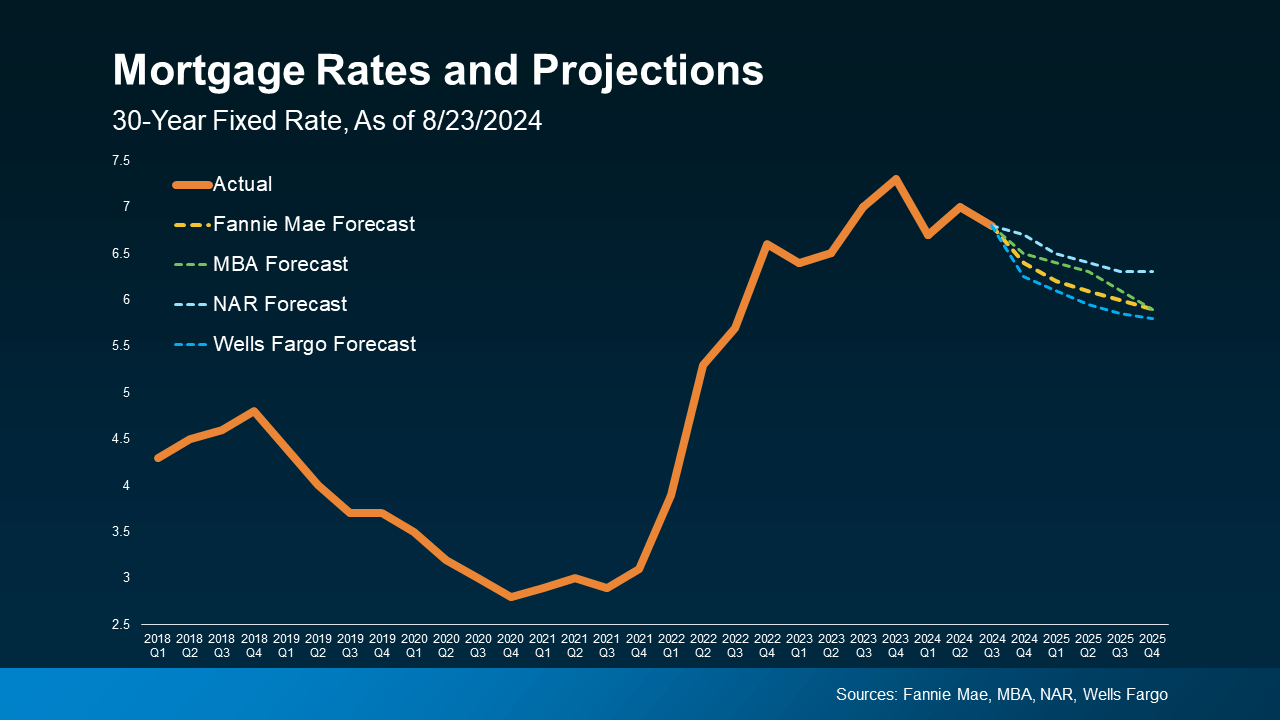

The Projected Impact on Mortgage Rates

Here’s what experts in the industry project for mortgage rates through 2025. One contributing factor to this ongoing gradual decline is the anticipated cuts from the Fed. The graph below shows the latest forecasts from Fannie Mae, MBA, NAR, and Wells Fargo (see graph below):

So, with recent improvements in inflation and signs of a cooling job market, a Federal Funds Rate cut is likely to lead to a moderate decline in mortgage rates (shown in the dotted lines). Here are two big reasons why that’s good news for both buyers and sellers:

1. It Helps Alleviate the Lock-In Effect

For current homeowners, lower mortgage rates could help ease the lock-in effect. That’s where people feel stuck within their current home because today’s rates are higher than what they locked in when they bought their current house.

If the fear of losing your low-rate mortgage and facing higher costs has kept you out of the market, a slight reduction in rates could make selling a bit more attractive again. However, this isn’t expected to bring a flood of sellers to the market, as many homeowners may still be cautious about giving up their existing mortgage rate.

2. It Should Boost Buyer Activity

For potential homebuyers, any drop in mortgage rates will provide a more inviting housing market. Lower mortgage rates can reduce the overall cost of homeownership, making it more feasible for you if you’ve been waiting to make a move.

What Should You Do?

While a Federal Funds Rate cut is not expected to lead to drastically lower mortgage rates, it will likely contribute to the gradual decrease that’s already happening.

And while the anticipated rate cut represents a positive shift for the future of the housing market, it’s important to consider your options right now. Jacob Channel, Senior Economist at LendingTree, sums it up well:

“Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever. Buy now only if it’s a good idea for you.”

The expected Federal Funds Rate cut, driven by improving inflation and slower job growth, is likely to have a positive, though gradual, impact on mortgage rates. That could help unlock opportunities for you. When you’re ready, let’s connect. That way you’ll be prepared to take action when the time is right for you.

Real Estate News •

September 12, 2024

The Great Wealth Transfer: A New Era of Opportunity

In recent years, there’s been a significant shift in how wealth is distributed among generations. It’s called the Great Wealth Transfer.

Historically, the transfer of wealth from one generation to the next was a more gradual process, often limited to smaller amounts of inheritance or family savings. But today, the scale has increased in a big way. As a recent article from Bankrate says:

“The biggest wave of wealth in history is about to pass from Baby Boomers over the next 20 years, and it’s going to have major impacts on many facets of life. Called The Great Wealth Transfer, $84 trillion is poised to move from older Americans to Gen X and millennials. If it’s managed smartly, Americans will be able to grow their wealth and ensure their financial security.”

Basically, as more Baby Boomers retire, sell businesses, or downsize their homes, more substantial assets are being passed down to younger generations. And this creates a powerful ripple effect that’ll continue over the next few decades. The graph below uses data from Merrill and Cerulli Associates to give you an idea of how much inherited money is set to change hands through 2045:

Impact on the Housing Market

One of the most immediate effects of this wealth transfer is on the housing market. Home affordability has been a concern for many aspiring buyers, especially in high-demand areas. The increase in generational wealth is expected to ease some of these challenges by providing future homeowners with greater financial resources. As assets are passed down through generations, buyers may find themselves in a better position to afford homes. Merrill talks about that benefit in a recent article:

“While millennials face steep barriers . . . to buying a first home in many markets, ‘that’s a for-now story, not a forever story’ . . . The Great Wealth Transfer should enable more of them to become homeowners — or trade up or add a second home — either through inherited property or the funds for a down payment.”

Impact on the Economy

But the Great Wealth Transfer doesn’t just impact housing. It’s also going to provide a new avenue for entrepreneurial spirits to fuel economic growth. If someone is looking to start a business and they’re receiving funds like this, that money can used as the necessary capital to start a new company. This helps the next generation of innovators and business owners bring their ideas to life.

While affordability remains a challenge in today’s housing market, the ongoing Great Wealth Transfer is poised to unlock new opportunities. As wealth is passed down and put to use, it’s expected to ease some of the barriers to homeownership and fuel other entrepreneurial endeavors.

Home Equity •

September 12, 2024

The Surprising Amount of Home Equity You’ve Gained over the Years

There are a number of reasons you may be thinking about selling your house. And as you weigh your options, you may find you’re unsure how you’re going to deal with one thing about today’s housing market – and that’s affordability. If that’s your biggest concern, understanding how much equity you have in your house could help make your decision that much easier. Here are two key factors that have a big impact on your equity.

1. How Long You’ve Been in Your Home

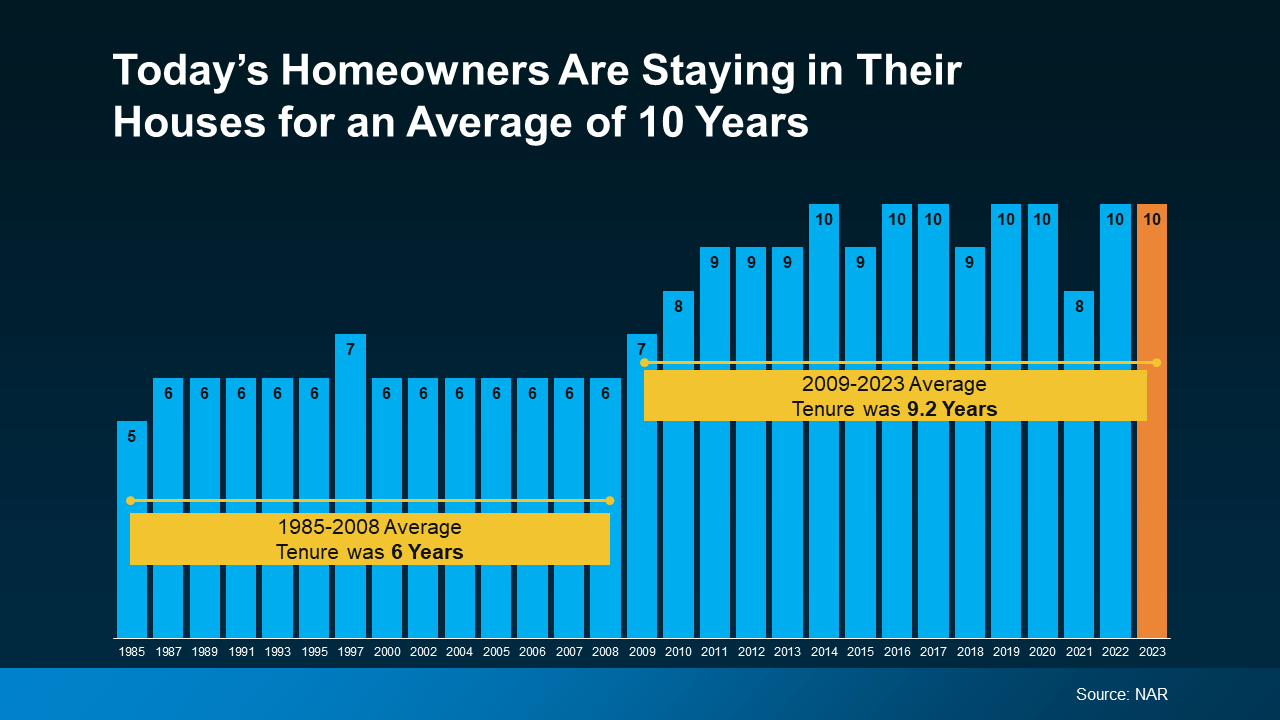

First up is homeowner tenure. That’s how long homeowners live in a house, on average, before selling or choosing to move. From 1985 to 2009, the average length of time homeowners stayed put was roughly six years.

But according to the National Association of Realtors (NAR), that number has been climbing. Now, the average tenure is 10 years (see graph below):

Here’s why that’s such a big deal. You gain equity as you pay down your home loan and as home prices climb. And when you combine all of your mortgage payments with how much prices have gone up over the span of 10 years, that adds up. So, if you’ve lived in your house for a while now, you may be sitting on a pile of equity.

Here’s why that’s such a big deal. You gain equity as you pay down your home loan and as home prices climb. And when you combine all of your mortgage payments with how much prices have gone up over the span of 10 years, that adds up. So, if you’ve lived in your house for a while now, you may be sitting on a pile of equity.

2. How Home Prices Appreciate over Time

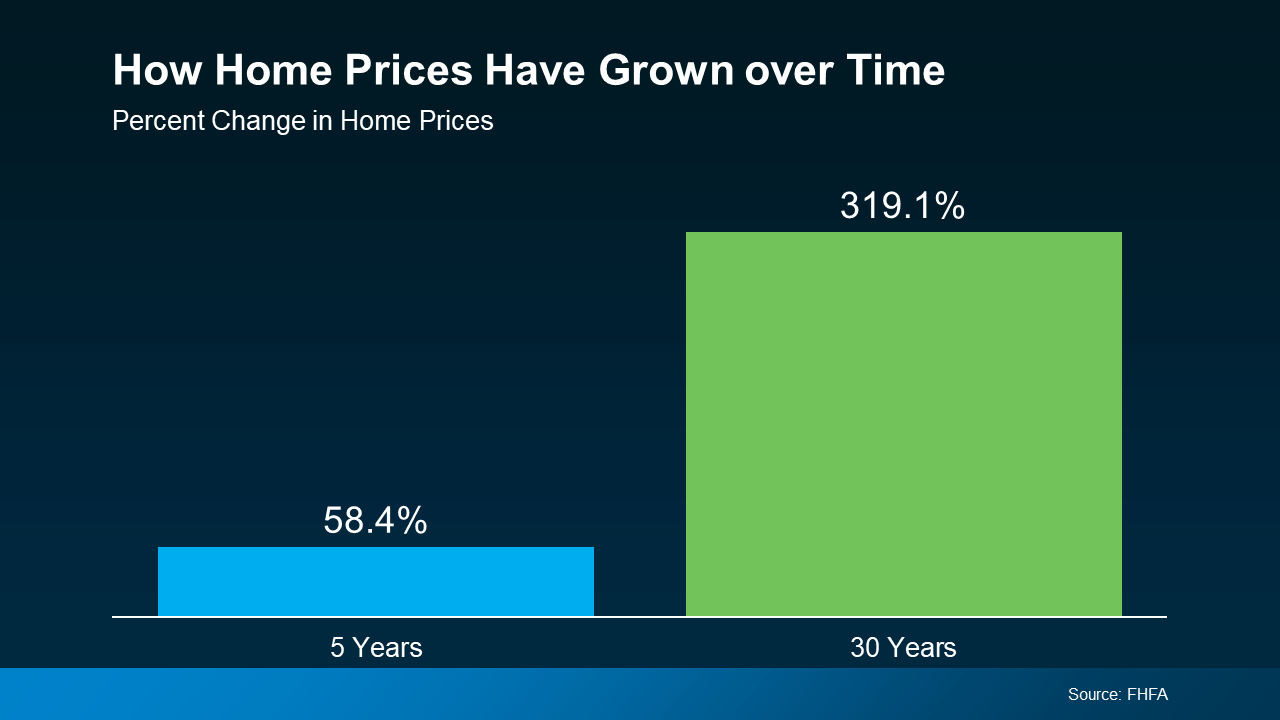

To help show how much the price appreciation piece adds up, take a look at this data from the Federal Housing Finance Agency (FHFA) (see graph below):

Here’s what this means for you. While home prices vary by area, the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it more than triple in value in that time.

Whether you’re looking to downsize, relocate to a dream destination, or move so you can live closer to friends or loved ones, your equity can be a game changer.

If you want to find out how much equity you’ve built up over the years and how you can use it to buy your next home, let’s connect.

Buying a Home •

September 12, 2024

Why Pre-Approval Should Be at the Top of Your Homebuying To-Do List

Since the supply of homes for sale is growing and mortgage rates are coming down, you may be thinking it’s finally your moment to jump into the market. To make sure you’re ready, you need to get pre-approved for a mortgage.

That’s when a lender looks at your finances, including things like your W-2, tax returns, credit score, and bank statements, to figure out what they’re willing to loan you. After that process, you’ll get a pre-approval letter to show what you can borrow. Here are two reasons why this is essential in today’s market.

Pre-Approval Helps You Know Your Numbers

While home affordability is finally starting to show signs of improving, it’s still tight. So, it’s a good idea to talk to a lender about your loan options and how today’s changing mortgage rates will impact your monthly payment. The pre-approval process is the perfect time for that. In addition to determining the maximum amount you can borrow, pre-approval also helps you understand this piece of the puzzle. As Investopedia says:

“Consulting with a lender and obtaining a pre-approval letter allows you to discuss loan options and budgeting with the lender; this step can clarify your total house-hunting budget and the monthly mortgage payment you can afford.”

You should use this information to tailor your home search to what you’re actually comfortable with budget-wise. Since mortgage rates have inched down some lately, you may find you’re able to afford a bit more than you’d expect for your monthly payment, but you still want to avoid overextending. As CNET explains:

“In many cases, a lender may preapprove you for more than you need to spend on a home. And while it can be tempting to look at houses outside your budget, it won’t help you in the long run. Before you start touring homes, figure out how much you can realistically afford and stick to your budget.”

Pre-Approval Makes Your Offer More Appealing

And once you do find a home you want in your budget, pre-approval has another big perk. It not only makes your offer stronger, it also shows sellers you’ve already undergone a credit and financial check. When a seller sees you as a serious buyer, they may be more attracted to your offer because it seems more likely to go through. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

As mortgage rates trend down, more buyers are going to be ready to jump back into the market. And while demand is still limited right now, there’s the potential for competition to pick back up, especially in hot markets. So, why not stack the deck in your favor and make sure you’re putting yourself in the best position possible when you find a home you love?

If you’re planning on buying a home, don’t forget to get pre-approved early in the process. It can help you get a more in-depth understanding of what you can borrow and shows sellers you mean business.

Buying a Home •

September 12, 2024

What To Know About Closing Costs

Now that you’ve decided to buy a home and are ready to make it happen, it’s a good idea to plan ahead for the costs that are a typical part of the homebuying process. And while your down payment is probably the number one expense on your mind, don’t forget about closing costs. Here’s what you need to know.

What Are Closing Costs?

Simply put, your closing costs are the additional fees and payments you have to make at closing. And while they’ll vary based on the price of the home and how it’s being financed, every buyer has these, so they shouldn’t be a surprise. It’s just that some people forget to budget for them. According to Freddie Mac, this part of the homebuying process typically includes:

- Application fees

- Credit report fees

- Loan origination fees

- Appraisal fees

- Home inspection fees

- Title insurance

- Homeowners insurance

- Survey fees

- Attorney fees

Some of these are one-time expenses that are baked into your closing costs. Others, like homeowners’ insurance, are initial installment payments for ongoing responsibilities you’ll have once you take possession of the home.

How Much Are Closing Costs?

The same Freddie Mac article goes on to say:

“Closing costs vary greatly depending on your location and the price of your home. Typically, you should be prepared to pay between 2% and 5% of the home purchase price in closing fees.”

Tips To Reduce Your Closing Costs

Costs can get pretty hefty, especially with today’s house prices, so I’ll work with you to find ways to lower costs when and where possible. Here are some ways that could help:

- Negotiate with the Seller: Some sellers are willing to cover part or all of these expenses — especially since homes are staying on the market a bit longer now. Sellers may be more motivated to compromise, and you’ll find you have a bit more negotiation power. So don’t hesitate to ask them for concessions like paying for the home inspection or giving you a credit toward closing costs.

- Shop Around for Home Insurance: Since rising home insurance is a challenge in many areas of the country right now, take the time to get a clear picture of all your options. Each insurance company offers their own policies and coverage, so get multiple quotes and see how they compare. Choosing a policy that provides reliable coverage at a competitive rate can make a difference.

- Look into Closing Cost Assistance: Just like there are programs out there to help with your down payment, options exist to get support with closing costs too. While they’ll vary by area, there are programs for various income levels, certain professions, and specific towns or neighborhoods too. If you want to learn more, Experian says:

“Your real estate professional should be able to steer you toward applicable programs, and the U.S. Department of Housing and Urban Development (HUD) maintains a helpful resource for finding homebuying assistance programs in every state.”

Planning for the fees and payments you’ll need to cover when you’re closing on your home is important – and it doesn’t have to be a big surprise. With the right experts on your side, you can make sure you’re prepared. Let’s connect so you have someone you can go to for more tips and advice.