Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Real Estate News •

June 17, 2024

Do Elections Impact the Housing Market?

The 2024 Presidential election is just months away. As someone who’s thinking about potentially buying or selling a home, you might be curious if the elections have an effect on the housing market. I was wondering the same thing, so thought I’d take a look to see what the data says.

Historically, presidential elections have only had a small, temporary impact on the housing market. Here’s the latest on exactly what’s happened to home sales, prices, and mortgage rates throughout those time periods.

Home Sales

During the month of November, in years when the Presidential election takes place, there’s typically a slight slowdown in home sales. As Ali Wolf, Chief Economist at Zonda, explains:

“Usually, home sales are unchanged compared to a non-election year with the exception being November. In an election year, November is slower than normal.”

This is mostly because some people feel uncertain and hesitant about making big decisions during such a pivotal time. However, the slowdown is only temporary. Historically, home sales bounce back in December and continue to rise the following year.

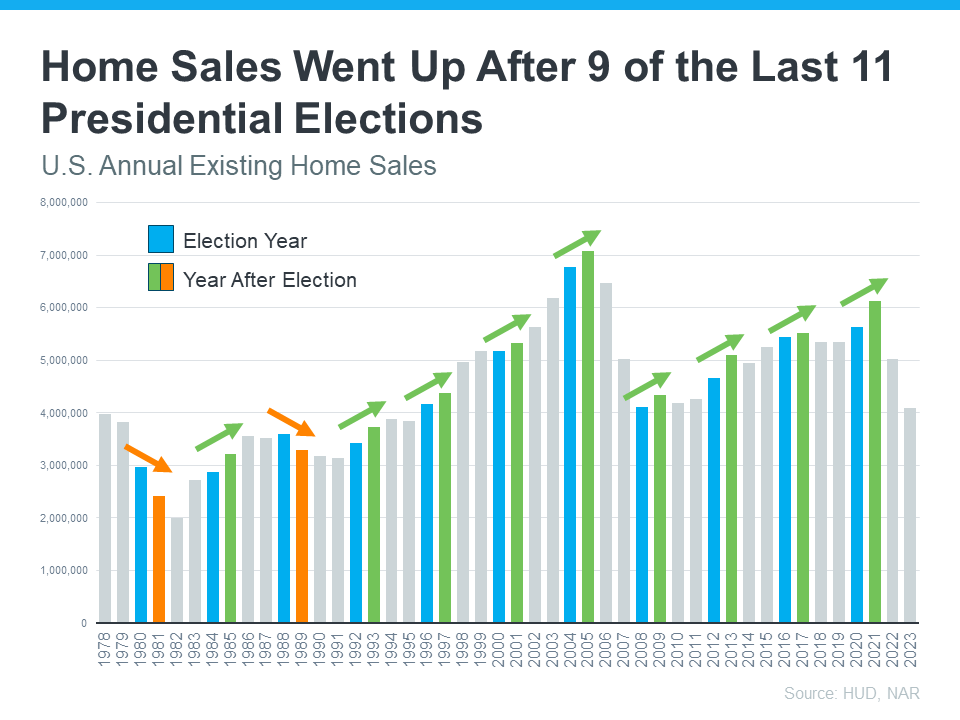

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after nine of the last 11 presidential elections, home sales went up the next year (see graph below):

The graph shows annual home sales going back to 1978. Each year with a presidential election is noted in blue. The year immediately after each election is green if existing home sales rose that year. The two orange bars represent the only years when home sales decreased after an election.

Home Prices

What about home prices? Do they drop during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist puts it:

“An election year doesn’t alter the price trend that is already happening in the market.”

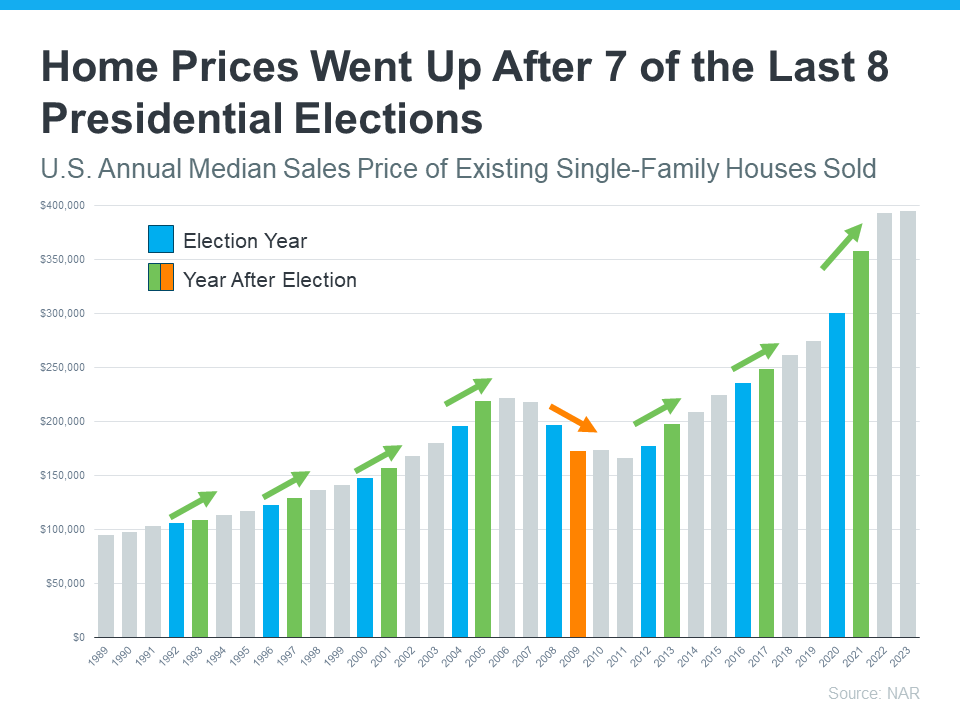

Home prices are pretty resilient. They generally rise year-over-year, regardless of elections. The latest data from NAR shows after seven of the last eight presidential elections, home prices increased the following year (see graph below):

Just like the previous graph, this shows election years in blue. The only year when prices declined after an election is in orange. That was during the housing market crash, which was far from a typical year. Today’s market is different than it was back then.

Mortgage Rates

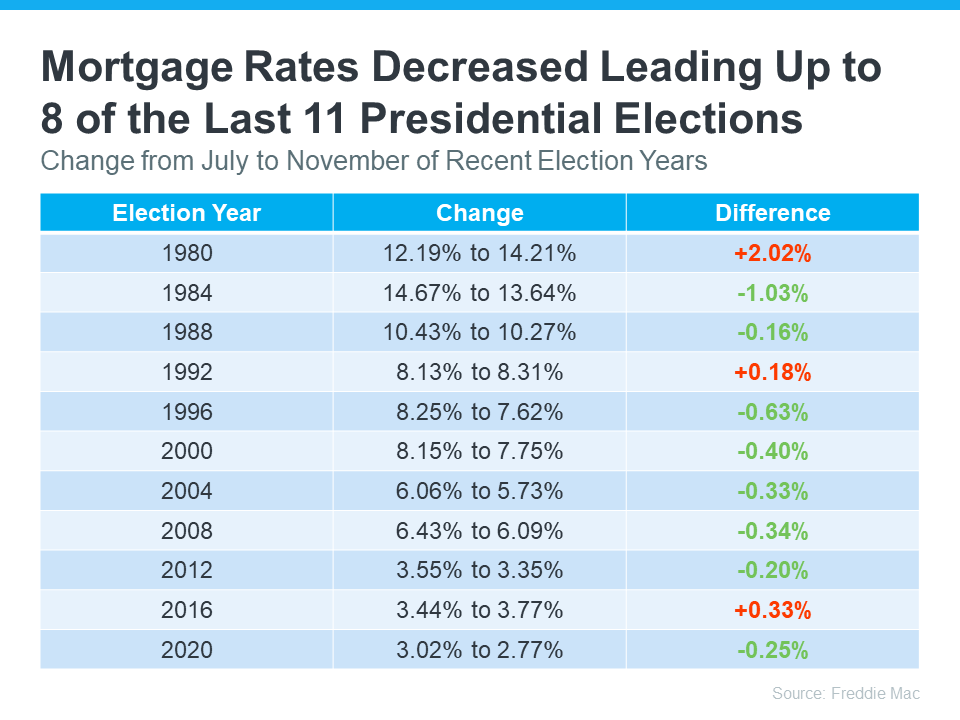

Mortgage rates are important because they affect how much your monthly payment will be when you buy a home. Looking at the last 11 presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in eight of them (see chart below):

Most forecasts expect mortgage rates to ease slightly throughout the remainder of the year. If they’re right, this year will follow the trend of declining rates leading up to most previous elections. And if you’re looking to buy a home in the coming months, this could be good news, as lower rates could mean a lower monthly payment.

What This Means for You

So, what’s the big takeaway? While presidential elections do have some impact on the housing market, the effects are usually small and temporary. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Seasonal Home Maintenance •

June 13, 2024

10 Home Maintenance Ideas for June

As summer kicks into gear, it’s the perfect time to tackle some essential home maintenance tasks.

With longer days and milder weather, why not take advantage of the favorable conditions to make sure your home’s in tip top shape! Here are 10 tasks that are perfect to do in June:

1. Check and Service HVAC Systems

If you have AC, make sure your system is in working order. Replace air filters, clean vents, and consider scheduling a professional service to keep your HVAC system running efficiently.

2. Inspect and Clean Gutters and Downspouts

After some pretty heavy spring rain, your gutters and downspouts might be clogged with debris. Clear them out to prevent water damage and ensure proper drainage away from your home’s foundation.

3. Examine the Roof for Damage

Take advantage of the clear weather to inspect your roof for any signs of damage, such as missing or damaged shingles. Addressing these issues early can prevent costly repairs down the line.

4. Service Lawn and Garden Equipment

Are your lawnmower, trimmers, and other gardening tools are in good working condition? Now’s the time to sharpen blades, change the oil, and replace any worn-out parts to keep your garden looking pristine all summer.

5. Check Carbon Monoxide Detectors

Carbon monoxide is a silent threat, and it’s vital to ensure your detectors are installed and working properly. Test each detector, replace batteries if needed, and install additional units if necessary to cover all living areas.

6. Clean and Inspect Windows and Screens

With more daylight hours, you’ll want to let in as much natural light as possible. Clean your windows inside and out, and check screens for any holes or damage. Repair or replace screens to keep bugs at bay while enjoying fresh air.

7. Pressure Wash Driveways and Walkways

Over time, dirt, grime, and mildew can accumulate on your driveways and walkways. Use a pressure washer to give these areas a thorough clean, enhancing your home’s curb appeal.

8. Inspect Exterior Paint and Siding

Examine the exterior of your home for peeling paint, cracks, or other damage. Touch up or repaint areas as needed to protect your home from the elements and maintain its appearance.

9. Check and Clean Dryer Vents

Lint buildup in dryer vents can pose a fire hazard. Disconnect the dryer, clean the vent thoroughly, and ensure there are no obstructions that could impede airflow.

10. Test Smoke Alarms

Alongside checking your carbon monoxide detectors, test all smoke alarms in your home. Replace batteries if necessary, and ensure each unit is functioning correctly to keep safe.

Keeping up with regular maintenance preserves your property’s value and ensures a safe and comfortable living space.

Buying Your Luxury Home •

June 5, 2024

The Sweet Spot for Buying Luxury Homes

If you’ve been looking for a home at the high end of your market, but haven’t found the right one, you may have put your search on hold. But according to recent data, now may be the time to jump back in. Here’s why.

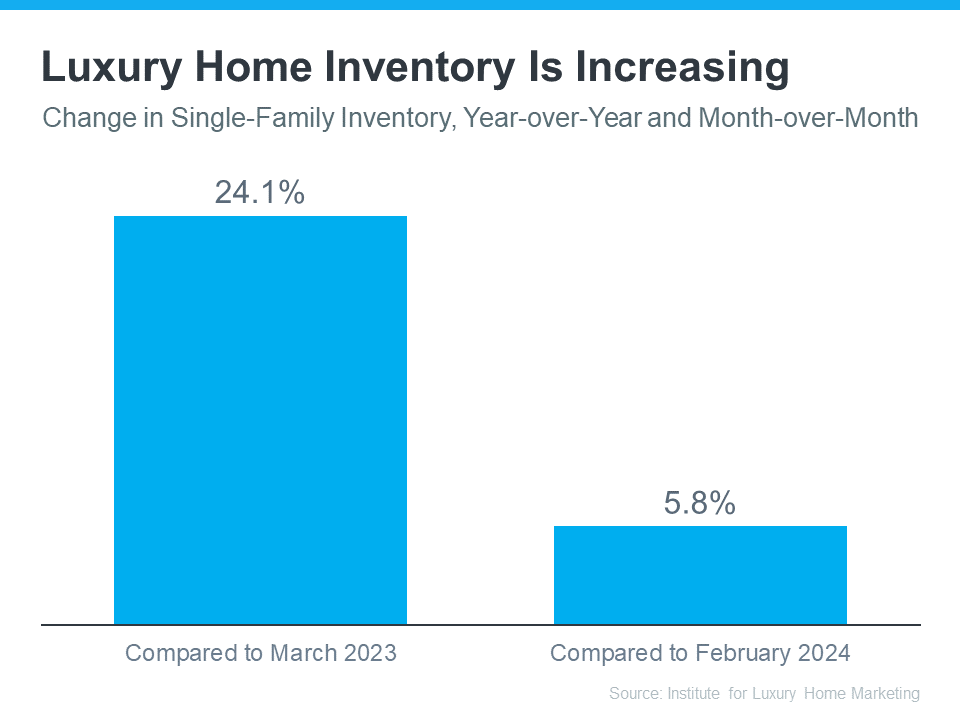

There Are More Luxury Homes To Choose From

What’s considered the top-end of the market, or a luxury home, will always vary by location. But generally speaking, they’re homes that are valued in the top 5% of any given market. According to a recent report from the Institute for Luxury Home Marketing, the selection of luxury homes is increasing

(see graph below):

As the graph shows, there are considerably more single-family luxury homes available now than there were a year ago. In fact, there are even more than there were just a month ago. This means you should have a wider variety of top-of-the-line homes to choose from, each with unique features and styles.

Whether you were searching for the latest design elements, like modern kitchens with chef-grade appliances, a breathtaking view, or integrated smart home technology, more luxury inventory means you should have an easier time finding one that matches your taste and lifestyle.

Rising Luxury Home Prices Can Help You Build Wealth

Another important factor to consider is that luxury home prices are on the rise. According to HousingWire, luxury home prices have increased by 8.7% over the past year. That’s why:

“People with the means to buy high-end homes are jumping in now because they feel confident prices will continue to rise . . . They’re ready to buy with more optimism and less apprehension.”

This means buying before prices climb higher – and while more inventory is on the market – may be your sweet spot. Because home prices are rising, owning a home could help you build more generational wealth over time. On the other hand, if you wait to buy, you might end up paying more for the same home later on as luxury prices continue to rise.

Bottom Line

With growing inventory and rising prices, you have a greater selection of luxury homes to choose from and an opportunity in front of you. Want to see the higher-end homes that are available in our area? Let’s connect today.

Selling Your House •

June 4, 2024

What To Expect if You Buy or Sell a Home This June

June is a busy month in the housing market because a lot of people buy and sell this time of year. So, if you’ve got a move on your mind and you’re looking to make it happen this month, here’s a snapshot of what you need to know to make sure you’re ready.

If You’re Buying This June

A lot of homebuyers with children like to move after one school year ends and before the next one begins. That’s one reason why late spring into summer is a popular time for homes to change hands. And whether that’s a motivator for you or not, it’s important to realize more buyers are going to be looking right now – and that means you’ll want to be ready for a bit more competition. But there is a silver lining to a move this time of year. This is also when more sellers will list – so you should find you have more options. As an article from Bankrate says:

“Late spring and early summer are the busiest and most competitive time of year for the real estate market. There’s usually more inventory listed for sale than other times of year . . . This is a double-edged sword for a buyer, as you will be met with more opportunities but [also] much more competition.”

During this busy season, it’s extra important to work with a trusted real estate agent. Your agent will help you stay on top of the latest listings, share expertise on how to make a strong offer in a competitive market, and give you insight into things like what the home is actually worth so you can make an informed decision when you buy. As Forbes says:

“Approaching the market confidently, armed with good information and grounded expectations will take you far. Don’t let the hustle of the market convince you to buy something that’s not in your budget, or not right for your lifestyle.”

If You’re Selling This June

Because there are more buyers this time of year, you’re in a great spot as a seller. Many of those buyers are highly motivated to make their move happen before the next school year kicks off – so they’ll likely put in strong offers to try to make that possible. That means, if your house shows well and is listed at market value, you could see your house sell faster or for a higher price. According to the National Association of Realtors (NAR):

“Warmer weather and the end of the school year encourage more people to buy and sell, respectively. Buyers are looking to move and settle before the new school year begins, contributing to increased competition and, consequently, higher prices.”

You want to be sure you’ve got a great agent on your side to help you with the contingencies on those offers and any negotiations that take place so you can pick the best offer. Make sure you go over closing dates with your agent. Buyers trying to time their move with the school year may need to delay a bit or move faster. This can depend on the school calendar where you live. As U.S. News Real Estate explains:

“ . . if your house goes under contract in early summer, the buyer may ask for a delay in closing or move-in until the school year finishes or their current home has sold. Alternatively, a buyer later in summer may be looking to close quickly and move in under a month. Remain flexible to keep the deal running smoothly, and your buyer may be willing to throw in concessions, like covering some of your closing costs or overlooking the old roof.”

So, if you’re looking to make a move this June, let’s chat so you know what to expect. We’ll come up with a plan that factors in current market conditions, but still works for you.

Homeownership •

June 3, 2024

More Than a House: The Emotional Benefits of Homeownership

With all the headlines and talk about housing affordability, it can be tempting to get lost in the financial side of buying a home. That’s only natural as you think about the dollars and cents of it all.

And while you ultimately need to be able to afford a home you buy, don’t lose sight of why homeownership was so important to you in the first place. That’s because buying a home is so much more than just a financial transaction. As the National Association of Realtors (NAR) says:

“The benefits of purchasing and owning your place of residence are both financial and emotional – pride in homeownership and the feeling of security are huge intangible benefits.”

Here’s a look at just a few of those more emotional or lifestyle perks, to help anchor you to why homeownership is one of your goals.

A Sense of Satisfaction

Owning a home is often associated with better mental health and well-being. That’s probably because buying a home is a big milestone. And the sense of satisfaction and pride that comes with achieving that goal just feels good. A recent article from the Mortgage Reports says:

“By and large, homeownership brings more satisfaction than renting. . . Surveyees scored the overall happiness level of homeowners at 88% compared to 67% for renters.”

More Stability for Your Family

Another thing that may make homeowners feel more satisfied is that they’re finally able to put down roots. Think about it. If you’re used to moving each time your lease renews and your rent climbs, staying put for a while would be nice not just for you, but for any loved ones that live with you.

A home can provide more predictability and the chance to make long-term friends. That should reduce everyone’s stress too. As NAR explains:

“Families also benefit from homeownership, with studies proving that parents are able to spend less time in a stressed state, therefore spending more time with their children. The ability for parents to feel stable has a huge impact on children’s behavioral issues, educational success, and future economic success.”

A Stronger Feeling of Community

And if you’re also looking for a sense of belonging for yourself, homeownership can help with that too. As FinHabits says:

“Homeowners tend to be more involved in their local communities, leading to a stronger sense of belonging . . .”

It makes sense. Your home connects you to your neighborhood and, by extension, your broader community. That’s because owning a home gives you a stake in that community’s future. So, becoming more involved and wanting to do what you can to help improve the area while making long-term relationships with neighbors is only natural.

The Ability To Make the Space Your Own

And don’t forget, your home is a place that’s all yours. Unless you’ve got specific homeowner’s association requirements, you’re free to customize it however you see fit.

So, if renting has been cramping your style, it’s time to express yourself and jump on the latest trends (if you want to). Whether that’s small home improvements or full-on renovations, your house can be exactly what you want and need it to be. And as your tastes and lifestyle change, so can your home. Picture coming home each day to a place that feels like you. That’s a feeling like no other.

Bottom Line

If you want to enjoy a sense of accomplishment and pride in where you’re living, let’s have a conversation to go over what you need to do now to make this future happen for you.

Selling Your House •

May 23, 2024

Questions You May Have About Selling Your House

There’s no denying mortgage rates are having a big impact on today’s housing market. And that may leave you with some questions about whether it still makes sense to sell your house and make a move.

Here are three of the top questions you may be asking – and the data that helps answer them.

1. Should I Wait To Sell?

If you’re thinking about waiting to sell until after mortgage rates come down, here’s what you need to know. So are a ton of other people.

And while mortgage rates are still forecasted to come down later this year, if you wait for that to happen, you may be dealing with a lot more competition as other buyers and sellers jump back in too. As Bright MLS says:

“Even a modest drop in rates will bring both more buyers and more sellers into the market.”

That means if you wait it out, you’ll have to deal with things like prices rising faster and more multiple-offer scenarios when you buy your next home.

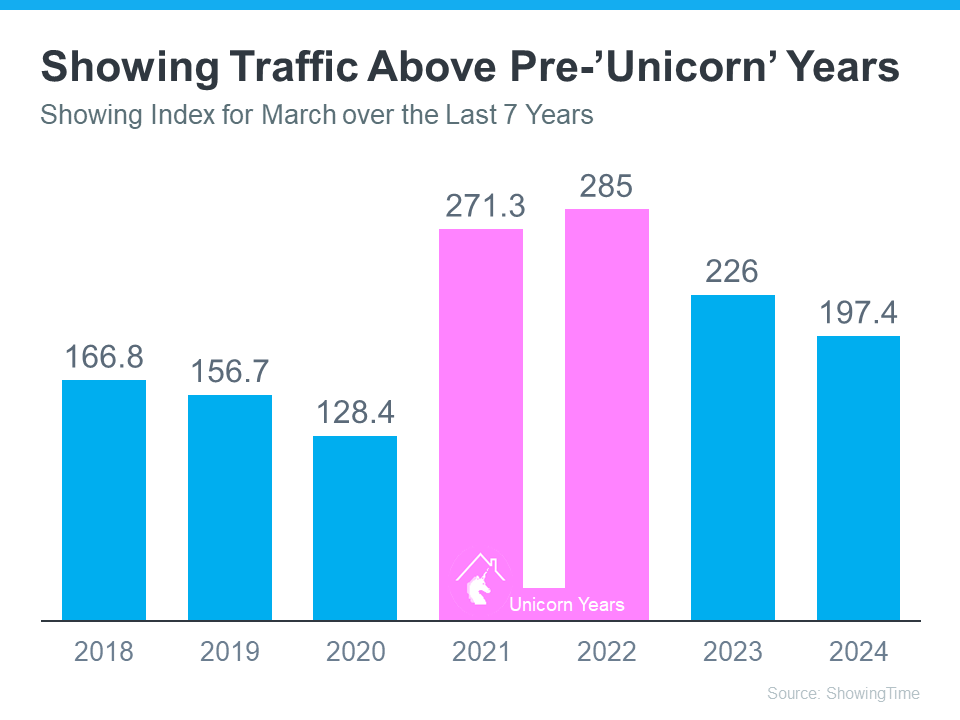

2. Are Buyers Still Out There?

But that doesn’t mean no one is moving right now. While some people are holding off, there are still plenty of buyers active today. And here’s the data to prove it.

The ShowingTime Showing Index is a measure of how frequently buyers are touring homes. The graph below uses that index to show buyer activity for March (the latest data available) over the past seven years:

You can see demand has dipped some since the ‘unicorn’ years (shown in pink). That’s in response to a lot of market factors, like higher mortgage rates, rising prices, and limited inventory. But, to really understand today’s demand, you have to compare where we are now with the last normal years in the market (2018-2019) – not the abnormal ‘unicorn’ years.

When you focus on just the blue bars, you can get an idea of how 2024 stacks up. And that gives you a whole new perspective.

Nationally, demand is still high compared to the last normal years in the housing market (2018-2019). And that means there’s still a market for your house to sell.

3. Can I Afford To Buy My Next Home?

And if you’re worried about how you’ll afford your next move with today’s rates and prices, consider this: you probably have more equity in your current home than you realize.

Homeowners have gained record amounts of equity over the past few years. And that equity can make a big difference when you buy your next home. You may even have enough to be an all-cash buyer and avoid taking out a mortgage altogether. As Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), says:

“ . . . those who have earned housing equity through home price appreciation are the current winners in today’s housing market. One-third of recent home buyers did not finance their home purchase last month—the highest share in a decade. For these buyers, interest rates may be less influential in their purchase decisions.”

Bottom Line

If you’ve had these three questions on your mind and they’ve been holding you back from selling, hopefully, it helps to have this information now. A recent survey from Realtor.com shows more than 85% of potential sellers have been considering selling for over a year. That means there are a number of sellers like you who are on the fence.

But that same survey also talked to sellers who recently decided to take the plunge and list. And 79% of those recent sellers wish they’d sold sooner.

If you want to talk more about any of these questions or need more information, let’s connect.

Buying a Home •

May 21, 2024

Worried About Home Maintenance Costs? Consider This.

If one of the main reasons you’re hesitant to buy a home is because you’re worried about the upkeep, here’s some information you may find interesting on both new home construction and existing homes (a home that’s been lived in by a previous owner).

Newly Built Homes Need Less Upfront Maintenance

If you can afford it, you may find a newly built home could help ease your worries about maintenance costs. Think about it, if everything in the house is brand new, it won’t have the wear and tear you may see in an existing home – and that means it’s less likely to need repairs. As LendingTree says:

“Since the systems, appliances, roof and foundation are new, you’re less likely to pay for major or minor repairs within the first few years of homeownership. That can make a big difference for first-time homebuyers who are adjusting to owning rather than renting.”

Plus, many builders also have warranties on their homes that would cover some of the more major expenses that could pop up. As First American explains:

“The new systems in your home, like plumbing, electrical, and HVAC, are typically covered for one to two years by your builder’s warranty. When something happens to these systems, you contact the builder or their warranty company.”

Existing Homes Can Still Have Great Perks

But it’s worth mentioning, that it’s not just newly built homes that can have warranties. It’s an option for existing homes too.

Your agent may be able to help you negotiate with the seller to add one as a concession on your contract. But you should know that not all sellers will be willing to do that. If they won’t, you could purchase one yourself, if you’d like to. An article from Forbes explains:

“During a real estate transaction, a home warranty policy can be purchased by the buyer or the seller.”

And there are benefits for both parties when it comes to a home warranty. According to MarketWatch:

“A buyer’s home warranty benefits both buyers and sellers, as it helps the seller close the deal while providing the future homeowner with peace of mind that they’ll be covered if a system or appliance breaks down . . . Sometimes, a seller will pay for the first year of the home buyer’s warranty to sweeten the deal, but it depends on the real estate market.”

If you’re interested in a home warranty for peace of mind, lean on your agent. They’ll negotiate on your behalf to see if a seller would be willing to cover one for you. Just remember, the likelihood of a seller throwing one in depends on conditions in your local market.

So, Should I Buy New or Existing?

While the need for less upfront maintenance is a great perk for new construction, there are some things a newly built home can’t provide that an existing home can.

For example, existing homes have a lot of character and charm that’s difficult to reproduce. The quirks that come with an older home may make it feel more homey. And, existing homes usually have more developed landscaping and a well-established sense of community. So, it can feel more inviting than something that’s a blank slate, like new construction often is. Not to mention, if you go with new construction, you may have to wait for the home to finish being built based on where it is in the process. It all depends on what’s most important to you.

Bottom Line

Whether you choose a newly built or an existing home, you may be able to ease some of your concerns over maintenance with a home warranty. To weigh your options and go over what’s the top priority for you, let’s talk.

Real Estate News •

May 20, 2024

What’s Next for Home Prices and Mortgage Rates?

If you’re thinking of making a move this year, there are two housing market factors that are probably on your mind: home prices and mortgage rates. You’re wondering what’s going to happen next. And if it’s worth it to move now, or better to wait it out.

The only thing you can really do is make the best decision you can based on the latest information available. So, here’s what experts are saying about both prices and rates.

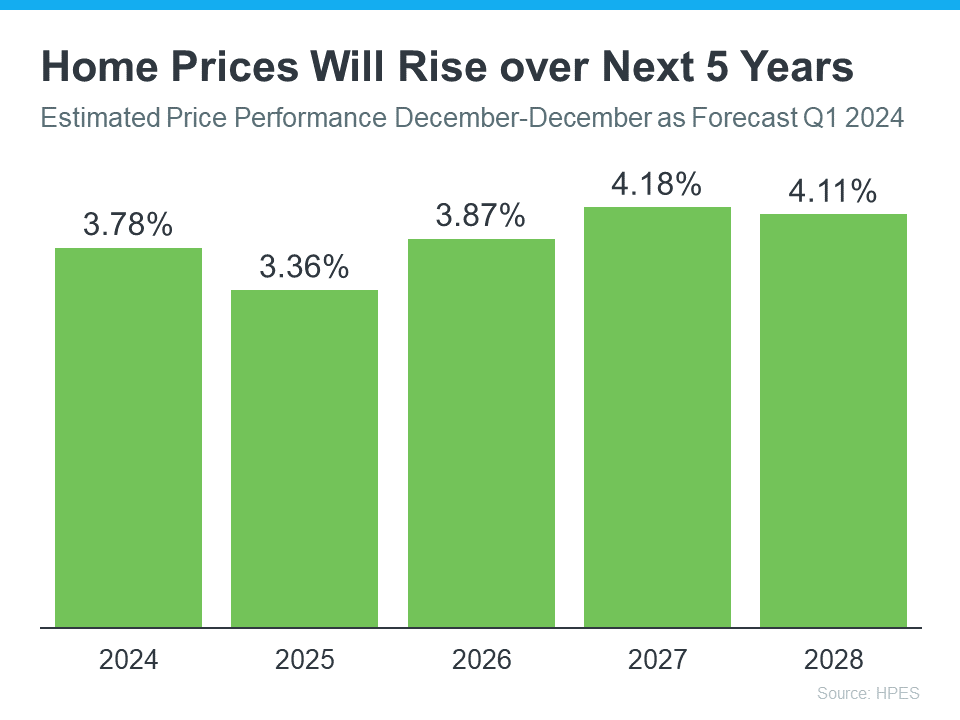

1. What’s Next for Home Prices?

One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts, and investment and market strategists.

According to the most recent release, experts are projecting home prices will continue to rise at least through 2028 (see the graph below):

While the percent of appreciation varies year-to-year, this survey says we’ll see prices rise (not fall) for at least the next 5 years, and at a much more normal pace.

What does that mean for your move? If you buy now, your home will likely grow in value and you should gain equity in the years ahead. But, based on these forecasts, if you wait and prices continue to climb, the price of a home will only be higher later on.

2. When Will Mortgage Rates Come Down?

This is the million-dollar question in the industry. And there’s no easy way to answer it. That’s because there are a number of factors that are contributing to the volatile mortgage rate environment we’re in. Odeta Kushi, Deputy Chief Economist at First American, explains:

“Every month brings a new set of inflation and labor data that can influence the direction of mortgage rates. Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

What happens next will depend on where each of those factors goes from here. Experts are optimistic rates should still come down later this year, but acknowledge changing economic indicators will continue to have an impact. As a CNET article says:

“Though mortgage rates could still go down later in the year, housing market predictions change regularly in response to economic data, geopolitical events and more.”

So, if you’re ready, willing, and able to afford a home right now, partner with a trusted real estate advisor to weigh your options and decide what’s right for you.

Bottom Line

Let’s connect to make sure you have the latest information available on home prices and mortgage rate expectations. Together we’ll go over what the experts are saying so you can make an informed decision on your move.

Buying a Home •

May 16, 2024

Tips for Younger Homebuyers: How To Make Your Dream a Reality

If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to buy a home? And chances are, you’re worried that’s not going to be in the cards with inflation, rising home prices, mortgage rates, and more seemingly stacked against you.

While there’s no arguing this housing market is challenging for first-time homebuyers, it is still achievable, especially if you have professionals on your side.

Here are some helpful tips you may get from a pro.

1. Explore Your Options for a Down Payment

If a down payment is your #1 hurdle, you may have options to give your savings a boost. There are over 2,000 down payment assistance programs designed to make homeownership more achievable. And, that’s not the only place you may be able to get a helping hand. While it may not be an option for everyone, 49% of Gen Z homebuyers got money from loved ones that they used toward a down payment, according to LendingTree.

And chances are you won’t need to put 20% down (unless specified by your loan type or lender). So be sure to work with a trusted mortgage professional to explore your options, find out how much you’ll really need, and learn about any guidelines on getting a gift from loved ones.

2. Live with Loved Ones To Boost Your Savings

Another thing a number of Gen Z buyers are doing is ditching their rental and moving back in with friends or family. This can help cut down your housing costs so you can build your savings a whole lot faster. As Bankrate explains:

“. . . many have opted to stop renting and live with family in order to boost their savings. Thirty percent of Gen Z homebuyers move directly from their family member’s home to a home of their own, according to NAR.”

3. Cast a Broad Net for Your Search

When you’ve saved up enough, here’s how a pro will help you approach your search. Since the supply of homes for sale is still low and affordability is tight, they’ll give you strategies and avenues you may not have considered to open up your pool of options.

For example, it’s usually more affordable if you consider a rural or suburban area versus an urban one. So, while the city may be livelier and more energetic, the cost of living may be reason enough to look at something further out. And if you consider smaller homes and condos or townhouses, you’ll give yourself even more ways to break into the market. As Colby Stout, Research Analyst at Bright MLS, explains:

“Being flexible on the types of home (e.g., a condo or townhome versus a single-family home) and exploring more affordable neighborhoods is important for first-time buyers.”

4. Take a Close Look at Your Wants and Needs

And lastly, an agent can help you really think about your must-have’s and nice-to-have’s. Remember, your first home doesn’t have to be your forever home. You just need to get your foot in the door to start building equity. If you want to buy, you may find making some compromises is worth it. As Chase says:

“An open-minded approach to house-hunting may be one way for Gen Z homebuyers to maintain some edge. This could mean buying in areas that are less expensive. Differentiating needs vs. wants may help in this area as well.”

An agent will help you prioritize your list of home features and find houses that can deliver on the top ones. And they’ll be able to explain how equity can benefit you in the long run and make it possible to move into that dream home down the line.

Bottom Line

Real estate professionals have expertise on what’s working for other buyers like you. Lean on them for tips and advice along the way. As Directors Mortgage says, with that support you can make it happen:

“The path to homeownership may not be a straightforward one for Gen Z, but it’s undoubtedly within reach. By adopting the right strategies, like exploring down payment assistance programs and sharing living costs with relatives, you can bring your dream of owning a home closer to reality.”

Let’s connect to get you set up for long-term success.